A comparison between the Dow Jones Industrial Average during the Spanish Flu Pandemic and the Covid-19 Pandemic. Continue reading

- Japan

- Market Indicator

- Price Momentum Indicators

- Richard Russell

- Silver

- Speed Resistance Lines

- U.S. Dividend Watch List

A comparison between the Dow Jones Industrial Average during the Spanish Flu Pandemic and the Covid-19 Pandemic. Continue reading

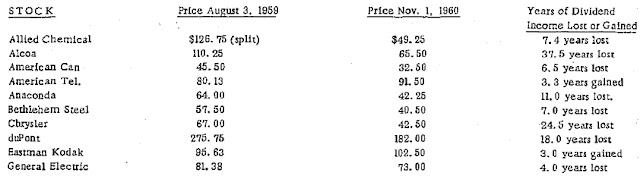

“Remember that the industrial and railroad stocks used in the averages are essentially speculative. Only to a limited extent are they held for fixed income by people to whom safety of the principal should be the main consideration, and their holders are constantly changing. If they were not speculative they would be useless for a stock market barometer. The reason why railroad stocks during 1919 did not share the bull market in the industrials was that, through government ownership and government guaranty, they had in a real sense ceased, for the time at least, to be speculative. They could not advance in any market, bull or bear, more than enough to discount the estimated value of that guaranty.”

-William Peter Hamilton, 4th Editor of the Wall Street Journal (The Stock Market Barometer. Harper. 1922. page 186.)

Government’s Impact on Risk

According to Hamilton:

“It is plain, then, that with a government guaranty of a minimum return, based upon the average earnings of three years ended June 30, 1917, the railroads entered the fixed income class (page 189.).”

-William Peter Hamilton, 4th Editor of the Wall Street Journal (The Stock Market Barometer. Harper. 1922. page 189.)

Many are arguing that the government purchase of assets along the widest spectrum of risk is the cause of a more speculative investing environment. The work of Hamilton, with the citation of rail stocks after nationalization, point to the opposite outcome, suggests that if the government is so influential then markets should become more sedated rather than increasingly restive.

Fannie Mae: The Evidence

The proof of the strength in the claims made by William Peter Hamilton can be found in the share price of the Fannie Mae and the 30-Year Treasury from 1977 to 2020.

As soon as Fannie Mae lost the implicit guarantee and achieved the actual guarantee of government support the share price has gravitated to tracking the 30-Year Treasury. The chart below shows Fannie Mae from 2013 to 2020 being unable to track beyond the 30-Year Treasury.

For now, Fannie Mae has become a bond even though it is possible to vacillate between $0.50 to $6.00 (+11,000% or -91.67%).

William Peter Hamilton

Often cited by Dow Theorists Robert Rhea and Richard Russell, Hamilton was an intense follower of the writings of Charles H. Dow, co-founder of the Wall Street Journal.

see also:

Dow Theory attempts to define and identify major moves in markets referenced here as the “primary trend.” In this piece, we will outline the price of gold according to Dow Theory.

We’re going to review and analyze the primary trend that extends from the September 2011 peak to the currently established low in the price of gold in December 2015. We believe that this information is critical to understanding where we are and where we might be going. This interpretation is based on the work of Charles H. Dow, co-founder of the Wall Street Journal and namesake to the longest continuous stock market indexes.

Keep in mind that all of the analysis that follows is done in generalities so that an individual who is curious about Dow Theory can refer to the technical manual on the topic titled The Dow Theory by Robert Rhea. However, the true heart of Dow’s theory is found in his original writing which covered the topic of earnings, dividends, effect of dilution of shares and economic outlook AND NOT lines on a chart. Two books that cover Charles H. Dow’s work as a fundamental analyst and an adept economist are titled Dow Theory: Unplugged and Charles H. Dow: Economist, respectively.

Lines on a Chart

Dow Theory has been synthesized down to a level of lines on a chart, which isn’t all bad. The lines still reflect fundamental economics. The challenge is the accurate interpretation of what is implied by the meaning of those lines.

NOTE: In our Dow Theory posting of May 18, 2014, we revealed an issue with Dow Theory that has gone unaddressed since S.A. Nelson’s book, The ABC of Stock Speculation, coined the term “Dow’s Theory.” We believe the acknowledgment of this issue adds clarity to the writings of Charles H. Dow and may produce new insights that have not previously been explored.

The question of retaining profits on quality dividend companies through the selling of a position seems to counter the whole point of dividend investing. After all, aren’t you supposed to allow the dividends to compound? In a small way, we described one approach and our rational for selling quality companies after small gains in yesterday’s article (Our Primary Concern: Retaining Profits).

However, there is another way to view the rationale behind selling a dividend stock after a “fair profit.” In the early years of the Dow Theory Letters, Richard Russell would often cite a Robert Rhea quote about the impact of a stock decline. Rhea said:

“’Buying in bear markets is merely gambling and not very good gambling at that. Why not have cash instead of investments in bear markets? Why insist that one cannot afford to forego investment income when one day’s price shrinkage may cancel several years’ dividends?’”

|

| Source: Richard Russell, Dow Theory Letters, http://www.dowtheoryletters.com/ |

Because stocks are not required to return principal with a stated yield as with many bonds, there is no assurance that the price will recover to the level that a purchase was initiated. Therefore, receiving short-term income on a dividend stock, although a necessary source of income for retired individuals, the prospect exists that an investor could end up with only a portion of the principal instead of the intended income plus principal.

The lack of assurance of principal and income with dividend stocks is why we believe people have become disenfranchised with technology stocks like Microsoft (MSFT) and Cisco Systems (CSCO). If they’ve invested in the stocks with the belief that they’re in it forever, when the decline comes, absent any dividend, there is little recourse or hope of recovering lost funds or keeping up with inflation.

Even new investors to Microsoft and Cisco Systems, aware of their bold promises in 1999 and subsequent failure to deliver in 2011, are asking themselves, “is it really worth facing the prospect of no return?” These questions are being asked when in some instances, especially with Microsoft, the timing probably couldn’t be better (especially now that they’re paying a dividend). Our supplementary comments on Microsoft can be found here.

While we subscribe to the Graham/Buffett principles of investing (buying for the long-term, you’re buying a business, concentrate on values, etc.) we assume that since there are only a handful of billionaires hewn strictly from investing in stocks, we might do well to hedge our thinking and strategy.

Finally, further analysis of Robert Rhea’s claim on not being invested at all during bear markets is something that is at odds with Charles Dow and we’ve decided is not appropriate or necessary. From our experience, bear markets are no guarantee of losses in your portfolio. Charles H. Dow, founder of the Wall Street Journal, has said that:

"Even in a bear market, this method of trading will usually be found safe, although the profits taken should be less because of the liability of weak spots breaking out and checking the general rise."

Schultz, Harry D., A Treasury of Wall Street Wisdom, Investors' Press, (New Jersey, 1966). p. 12. Additional commentary here.

Evidence of the fact that bear markets don’t always equal destruction of wealth, while going long stocks, is demonstrated in our 2007, 2008 and 2009 performance review. Naturally, 2008 is not expected to be replicated (having gains, while going long only, during a market decline of 40% or more). However, we do know that being all in or timing the market to be all out during bear markets shouldn’t be the goal. The goal, from our perspective, should be the preservation of gains whenever possible.

Posted in CSCO, Dow Theory, Harry Schultz, MSFT, Richard Russell, Robert Rhea

Posted in book, Dow Theory, Robert Rhea