In its heyday, Wilmington Trust (WL) garnered considerable respect in the wealth management industry. In fact, Wilmington Trust had increased its dividend for 27 years in a row until April 2009. Wilmington, a wealth management firm with a growing banking presence, became mired in troubled real estate construction loans that went bad as the financial markets unwound in 2007. After a TARP injection of $330 million and a capital raise of $274 million, Wilmington found itself in need of a savior.

In an October 16, 2010 article in Barron’s titled “A Bank on the Brink” by Erin Arvedlund, the future prospects of Wilmington Trust (WL) are covered in great detail. At the time of the article, Wilmington Trust was trading at $7.79. Barron’s asked Dick Bove banking analyst for Rochdale Research and Andy Stapp of B. Riley and Co. their view on the prospects for Wilmington Trust.

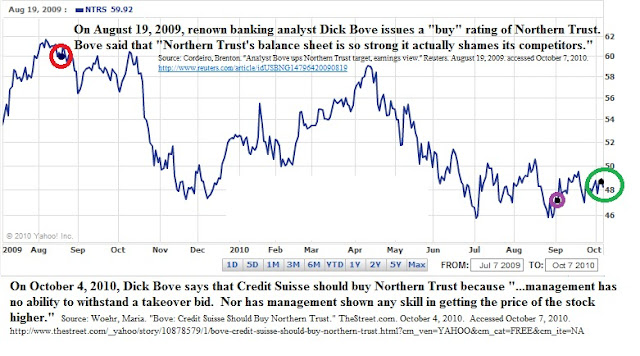

Dick Bove indicated that Wilmington Trust (WL) management “would rather shoot themselves than sell” to another institution, adding that “they may have no choice.” Bove said that Northern Trust (NTRS), a company profiled as an Investment Observation on our site, was among the potential acquirers of Wilmington. In the final analysis, Bove said that whoever ends up buying Wilmington Trust would have to “have faith” that the financials were accurate and that “it’s a crap shoot” for anyone to consider Wilmington.

Andy Stapp, senior analyst at B. Riley and Co. seemed to have a more optimistic view on Wilmington Trust (WL) saying that only a minority interest was likely to be sold at around $9 to $11 per share. Despite his belief that Wilmington Trust could possibly sell at a premium of 13%-39% above the market price, Stapp did hold off issuing a buy recommendation of the stock until the November 1st earnings release.

On October 25, 2010, in an article titled “Wilmington Trust Stock Slides,” TheStreet.com discussed the prospects of Wilmington Trust (WL). According to Janney Montgomery Scott analyst Stephen Moss, Wilmington Trust could be acquired for $8 per share but would not be surprised if the company sold for “substantially less.”

On November 1, 2010, it was announced the M&T Bank (MTB) would acquire Wilmington Trust for $3.84 per share, a discount of 46% below the closing price of October 29, 2010. According to a ThomsonReuters news article titled “M&T Bank Snaps Up Bargain-priced Wilmington” the shares of Wilmington Trust were being bought based on the tangible book value of the company at the end of September 2010. Almost overnight, the price of Wilmington Trust (WL) was cut in half.

Final Observations:

- Bove was right, WL was a crap shoot at $7.79

- Stapp was wrong, WL was not nearly worth $9

- Tangible book value is a good starting point for research

- Always be prepared for the market price of a stock to be cut in half