Recently, in an article titled “

Sell Signal for Stocks” found in

Barron’s, Michael Kahn covers the topic of Dow Theory. The subtitle to the article was “

a big drop in the transportation sector killed hope for a Dow Theory buy signal.” To the untrained reader of Dow Theory, Kahn’s article seems harmless enough. However, there are significant issues that need to be reconciled before it can be considered a discussion of Dow Theory.

Getting down to business, there are a couple of items that have to be addressed starting with the subtitle. First is the part that says “a big drop in the transportation sector killed hope for a Dow Theory buy signal.” If you’re someone who wishes to practice Dow Theory, you must abandon all hope, literally. William Peter Hamilton once said:

“The averages, indeed, must be read with a single heart. They become deceptive if and when the wish is father to the thought”[1].

For Mr. Kahn to imply that hope has a role in a Dow Theorist’s mind when a buy signal is registered suggests that Mr. Kahn doesn’t understand Dow Theory. The study of the market using Dow Theory is best done when hopes and fears are abandoned.

The second item of concern in the subtitle relates to the indication of a buy signal. Dow Theory isn’t a “beat the market” strategy or get rich scheme. Dow Theory is as much an indicator of future economic growth for our country as it is a barometer for the stock market. William Peter Hamilton shed light on this topic by saying:

“Diligent study of the averages will sufficiently show where a ‘line,’ having proved to be one of accumulation, has given definite information, not merely useful to the trader but valuable to those who look upon the stock market as a means of forecasting the trend of the country's general business”[2].

Also, Dow Theory does not give buy or sell signals. As a barometer, it merely indicates the direction that the stock market and economy might go three to nine months into the future. Those who take bull market indications as buy signals still need to be well versed in understanding values and its role in the selection of stocks. If a person not versed in values believes that a bull market indication means that they can haphazardly buy stocks then they are most likely to suffer severe losses and quickly become disenchanted with investing in stocks.

Throughout Kahn’s stab at Dow Theory, statements like “…good times turn to bad…” and “…followers of the century-old Dow Theory suddenly got excited” or “…followers were eagerly awaiting…” suggests that a person who uses Dow theory is emotionally tied to the outcome. Charles H. Dow was about as unemotional on the markets as anyone could get. William Peter Hamilton couldn’t become editor of the Wall Street Journal until after Dow’s death because Dow thought that Hamilton was too emotionally tied to his work. A person who is involved with Dow Theory needs to check their emotions at the door. Mr. Kahn seems to not take this into consideration when he wrote his article. If anything, Mr. Kahn should only be following Dow Theorists who reflect the most balanced view on the market’s direction, either up or down.

Specific to Dow Theory, Kahn says something that jumps off the page. In the fourth paragraph, Kahn states, “The bears have apparently resumed control of the stock market…” Kahn arrives at this conclusion based solely on the fact that the Dow Jones Transportation Index has declined. In Dow Theory, there is no such reference to the idea that simply because a single index declines from a peak that a bear market has been registered or that “the bears have resumed control of the stock market…” At no point does Kahn reference the fact that the prior trend (bullish) is presumed to be in force until specific conditions are met. Hamilton says as much in the following remark:

“Perhaps it might be permissible to say that the secondary [reaction] movement suspends for a time the great primary swing, although a natural law is still in force even when we counteract it”[3].

Richard Russell adds clarity to Hamilton’s comments by saying the following:

“… in examining the action of the Averages over a period of sixty-five years, the Dow Theorist has learned, among other things, that the movement of a single Average should never be considered alone. Further, the Dow Theorist has learned that the last trend should be considered to remain in effect until the contrary has been proved”[4].

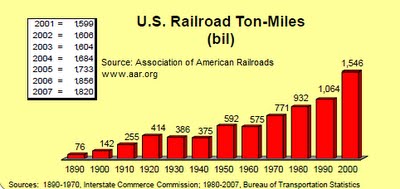

In the sixth paragraph, Kahn suggests that because the composition of the Dow Jones Industrial Index has changed dramatically over the years that we could hardly expect it to be a true reflection of our economy. Kahn implies that because we’re in a services and information-based economy, that there is less transporting of products by rails and trucks and therefore can’t possibly be reflective of the times. The charts below reflecting only the rail sector tells a completely different story.

For 2007, more revenue was generated through rail transportation than any other method of domestic transportation. Not far behind rail was trucking, which, when combined, equaled nearly 74% of total revenue generated for all methods of transportation within the U.S.

In paragraph 7, Kahn succumbs to a common myth about the relationship between commodity prices and the level of the stock market. Kahn suggests that when commodity prices are down then the stock market has every reason to rise because commodities “…are input costs for many large-cap U.S. companies…” Certainly commodities are input costs for most production but there is little to suggest that there is an inverse relationship between the two other than the ebb and flow of bad U.S. monetary policy. As a Dow Theorist, Kahn should know that Charles H. Dow said in his Wall Street Journal column on February 21, 1901:

“…the stock market and the commodity market move substantially together” [5].

We have been able to confirm the relationship between commodity prices and the stock market with

gold, silver and various commodity processing companies like

ConAgra (CAG), Heinz (HNZ),

Archers Daniels-Midland (ADM) and

Sysco Foods (SYY). Kahn is right about the input costs but wrong about the inverse relationship between the stock market and commodities.

Starting in paragraph 9, Kahn begins to provide technical analysis of the iShares Dow Jones Transportation ETF. Use of an ETF to derive inference of the Dow Jones Transportation Average when the data on the index is freely available comes off as lazy. In the end, the ETF cannot show you what the Dow Jones Transportation Average did in 1946 or 1973 which is important because inevitably you’re going to need that data. If Kahn was going to use the Tranports ETF, he should have shown the 100% correlation to the actual index to justify using the ETF. No such evidence was presented for using the ETF over the actual index.

In the review of the transport ETF, Kahn speaks at length on chart patterns known as gaps and gap reversals. Considerable effort is put into explaining how the gap reversal pattern reflects negatively on the direction of the transport ETF. However, noticeably absent in his discussion of the transport ETF is the obvious “double top” formation. Double tops and double bottoms were indicated to be very important formations according to Charles H. Dow. Alternatively, William Peter Hamilton and Robert Rhea arrived at the conclusion that such formations bear little importance when considering the price movement of the indexes. From our own work on the topic of double tops and double bottoms, we have found that Dow was right about the importance of such a price characteristic and have been able to prove, with

significant evidence throughout the history of the Dow indexes, that double tops and double bottoms are critical indicators for determining market direction when applying Dow Theory.

After the discussion of the transports ETF, Kahn goes far afield when he starts to discuss the price action of several illiquid sector specific ETFs from within the transportation industry. Kahn covers the airline and shipping as representative examples of the malaise that he believes reflects the weakness in the transportation sector of the economy. Both the airline and shipping ETFs are reaching new 52-week lows (our favorite point to examine values.) However, such analysis doesn’t seem to add up when compared to the iShares Dow Jones Transportation ETF.

If the Dow Transportation ETF is just coming off of a new high, then what relevance does the airline and shipping ETFs have to do with the discussion of the broader index which contains shipping, rail and airline stocks? From a Dow Theory perspective, such maneuvering to prove a point is in contravention of the theory itself. According to Dow, Hamilton, Rhea and a host of others, though not infallible, the averages discount everything.

Kahn finishes his article by saying that if the Dow Jones Transportation Average (notice the switch to index from the ETF) cannot hold above the March low of 4920 then a sell signal would have been registered. Dow Theory just doesn’t work this way. The theory is all about confirmations. As Hamilton says:

“One of the shortest ways of going wrong is to accept an indication by one average which has not been clearly confirmed by the other. [6]”

If the Transportation Average breaks the March low then the only way to get a sell signal is to have the Industrial Average break the March low. For all intents and purposes, the Transportation Average could fall to 3000 or lower without triggering a sell signal. Historically speaking, such a wide divergence on a relative basis has occurred before without triggering a sell signal.

We understand that Kahn is the big money man who can articulate his thoughts in a fashion that is acceptable to publications like Barron’s. However, we know that his interpretation of Dow Theory is incorrect.

Citations:

[1] Hamilton, William Peter.

The Stock Market Barometer. Harper & Brothers, New York. 1922.

page 133.

[4] Russell, Richard. Richard Russell’s Dow Theory Letters. Issue 166. December 27, 1961. page 1.

[5] Sether, Laura. Dow Theory Unplugged. W&A Publishing. 2009. page 50.

[6] Hamilton, William Peter.

The Stock Market Barometer. Harper & Brothers, New York. 1922.

page 138.

Please consider donating to the New Low Observer. Thank you.