We have frequently claimed that our goal was never to have trading strategy while dealing with dividend paying stocks. In fact, the whole purpose of mining the field of dividend stocks is to increase the odds that we can compound our investment income.

However, a recent example reminds us of the importance of being cognizant that “good” stock selecting isn’t enough. Adherence to Charles H. Dow’s concept of recognizing values and seeking fair profits is critical to long-term success in the stock market.

In the article titled “When Timing Meets Opportunity,” we’ve outlined the importance of timing when selecting stocks. That article demonstrated that a focus on stocks near a new one-year low was about as good as any time for starting investment research. Stocks at a new low represent the best marker for determining values. Keep in mind that our focus is on stocks that increase their dividend every year or members of the Nasdaq 100. Thereafter, an individual would need to run through whichever fundamental and technical analysis necessary to make a decision that seems appropriate. Our philosophy is to consider our portfolio allocation based on what Dow Theory indicates. If we’re in a bull market we have a higher concentration in a single stock. If we’re in a bear market then we have lower concentration in a single stock. In general, this addresses the “value” component according to Charles H. Dow.

The aspect regarding seeking fair profits, another Charles Dow tenet, was outlined in our article titled “Seeking Fair Profits in Investment Portfolios.” That article specifically references quotes by Charles Dow regarding when to take a profit on a stock. Strangely, Dow recommended taking “fair profits” of 5%. The New Low Observer Team is a little more adventurous since we seek 10% or more. However, the point remains that as investors we need to put our expectations in perspective before we commit our money. Not after we’re stuck with large gains or losses.

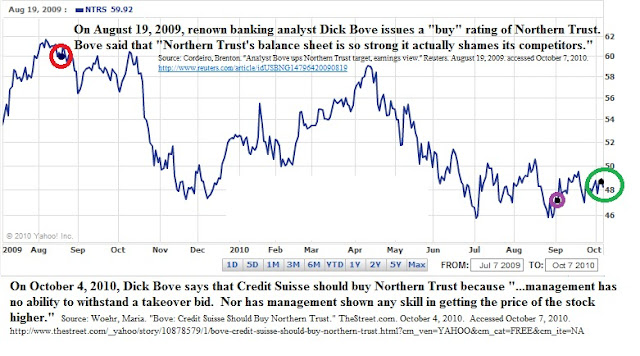

A recent example that we have come across is the case of Northern Trust (NTRS). Northern Trust (NTRS) typifies what usually happens to a well-timed play on values when the appreciation for “fair profits” isn’t understood. Northern Trust was recommended on September 1, 2010. This was almost literally at the one year low from the period of September 1, 2009 to September 1, 2010.

After receiving “only” 10.96% in a period of 64 days, we issued a Sell recommendation on Northern Trust (NTRS) feeling that an annualized gain of nearly 40% wasn’t worth quibbling about. In the sell recommendation, we indicated that we expected the upside target to be first $56 and thereafter $59. Almost as impossible as it seems, Northern Trust peaked at $56.86 and turned down from there. Nearly 7 months on, Northern Trust (NTRS) has ranged from a 19% gains to the current 4%. In addition, this represents a loss of nearly half of the gain that was generated at the time of our sell recommendation.

The situation with Northern Trust typifies our experience and observation when investing in dividend increasing stocks. Great companies with considerable qualitative elements rise for a moment and revert back to their prior low for inexplicable reasons. In regards to the general ebb and flow of individual stocks, we’re primarily concerned with accepting what is reasonable and fair rather than what we typically want which is usually for the stock to got back to the previous one-year high.

As rudimentary as it seems, we feel that an understanding of values and seeking fair profits, as espoused by Charles Dow, is essential to long-term success in the stock market.

- Another great example that illustrates our point more graphically is in the article titled “Gaining More by Limiting our Gains.”