The following is a response by a reader regarding the February 8, 2010 article outlining all of the transactions from 2008:

1) You had 94% of all investable funds in Wesco at one time which to me appears extreme concentration in one asset class, regardless of how confident one is about the prospects. And since the future is unpredictable, I believe the risk/reward outcome unnecessarily becomes a hostage to the "Black Swan" events.

I do note that you had a timely and efficient loss control mechanism in place and that you sold out at a minimal loss. But that might be because you had such a huge overweight in that one stock, forcing you to watch it like a hawk. Had it been a small weight, you might have acted differently, even not having sold out and thus made a much greater profit in absolute terms since Wesco climbed 10% to 15% higher soon after you sold it.

This is a good example of why single, huge overweight concentration in one security is generally counterproductive because we are forced into taking quick actions based on short term volatility and transient perceptions of risk.

2) Almost ten times out of a total of 40 trades you let your realized losses exceed 10% and in one case even go as high as 46%. I am not averse to enduring high unrealized losses in special cases wherein we are convinced about the intrinsic value of the investment, and are willing to "ride out the storm". This is a part of the process of investing. However, I wonder what intrinsic value, or a miraculous turnaround, you were seeing holding Fannie May during the summer and early fall of 2008. Granted, you had a small allocation to this name at the time, but the expectations surrounding this trade appear to me to be speculative in nature.

3) After September every trade was a losing trade (except the three with small profits), all the way through the end of the year. And that was not in the least unusual, since being in the stock market was simply not the right strategy at the time. I am not sure what the Dow Theory was telling us around this time -- during this period of extreme volatility and spreading risks throughout the investment landscape globally. Maybe you can throw some light with respect to the Dow Theory in this context, for this period. And also whether any other asset allocations were considered and rejected. (For instance, 4Q08 provided bountiful profits in the Treasury bonds with minimal volatility and low risk.)

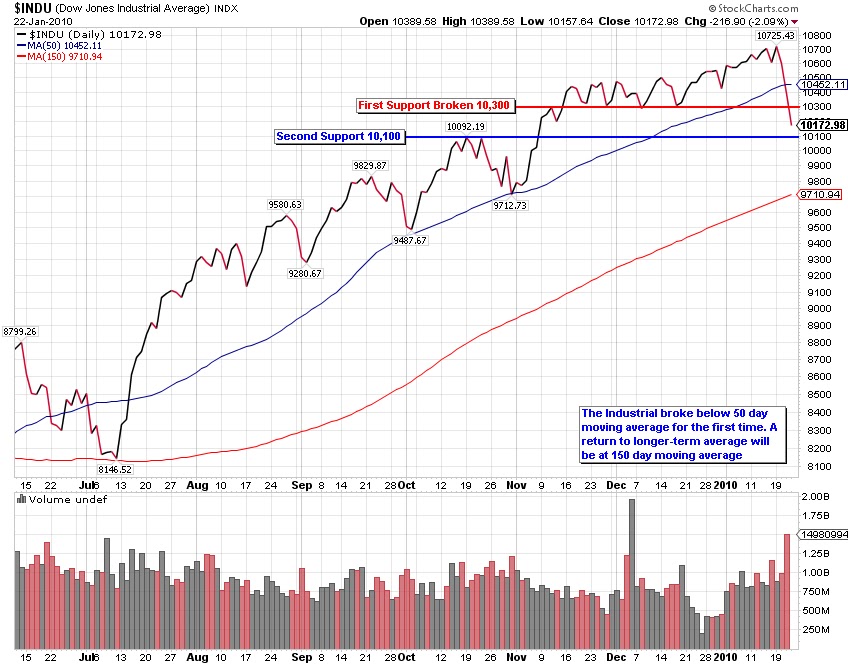

“Today the Dow Jones Industrial Average has fallen to the minimum of 9525.32. This exceeds the Dow Theory projection of 9531.11 posted on this blog on September 17, 2008. Nothing that has happened thus far is surprising according to Dow's Theory. It becomes academic at this point to suggest that we are either going to the 7197.60 level…”

“After today's stock market action the Dow Jones Industrial Average closed at the level of 10,609.66. This is below the 50% Principal as devised by E. George Schaefer. The 50% principal indicates that if a stock or index falls below this level it will fall, at minimum to the 2/3 level of Dow's Theory. Right now the 2/3 level for the Dow Jones Industrial Average is 9531.11. If the Dow falls below the 2/3 level the next stop will be 7,197.60.”

{kind=link}

{kind=link}

Market Commentary

Comments Off on Market Commentary

Posted in Commentary, fair profit