We at New Low Observer are constantly challenging our own method of investing. We often ask "how is it possible that a great stock like that can be down/up that big?" To answer that question, we looked at what could be a potential explanation and we turned to our trade on H&R Block (HRB).

Buy Recommendation from the "Pro" in 2008

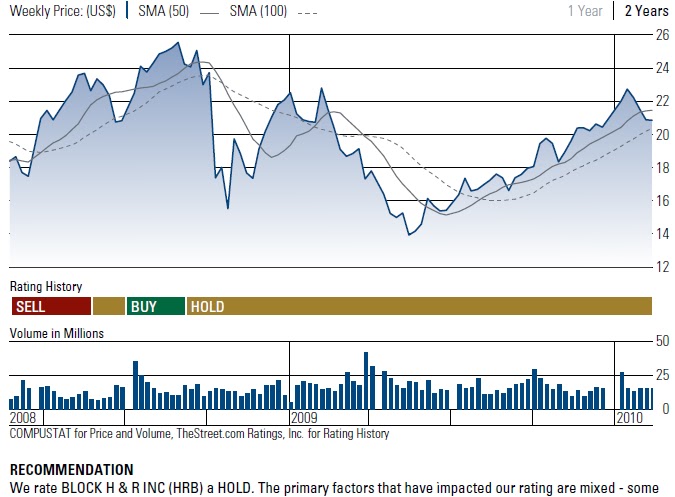

The chart below shows a buy recommendation from TheStreet.com. They upgraded HRB from hold to buy on July 1, 2008 at $21.08. Then TheStreet told investors to hold it on September 5, 2008 at $24.24. At the current price, it would take a 40% rise (from $17.20 to $24.24) to break-even.

We began our coverage of HRB on May 19, 2009 when the stock was trading at $14.42 or 5% within the 52-week low of $13.73. Please see chart below.

Our article was published on Seeking Alpha which received less than welcomed comments. One reader stated:

"HRB's core business is doing tax preparation. People are moving to doing it via a computer. They are losing core business and been doing so for years. You sure you want to invest in a company losing its core?"

The other came from a former employee. He provided us with great insights:

"As a former employee, I can tell you that this ship has sailed. Every article you read that talks about an upside merely mentions shedding the toxic business, (Business that by the way doubled the profits for a number of years), but fails to mention the drop in repeat clients. If this any other retailer, the first thing you would look at is same store sales YOY and ignore entities that they no longer own. Same store sales are dismal and this year were down close to double digits. This year when they could have been the client's champian with wallets tight, they raised the average fee by nearly 9%. The 5.6% drop in clients includes a 10% increase in digital clients where the profit margin is razor thin.

Every year it is a push to pick up new clients and that is harder than ever. The clients they need to pick up are the thirty-somethings who grew up in the computer age and are very comfortable with a software solution. Good luck because they are also reluctant to pay $300.00 to have their taxes prepared by someone that they are not convinced is smarter than they are.

If you own it, hold it until Breedan sells the company and if you don't, don't."

Based on these comments, one might have considered HRB to be doomed. The stock had nowhere to go but down. But wait...

To our surprise, in just 17 days, HRB rose a little over 10% by June 5, 2009. We didn't expect to garner such a large profit in such a short period of time. Because our goal is "seeking fair profits" we had to recommend selling the shares.

Investors should be asking, how can HRB rise 10% during a period with no news and such a negative outlook based on comments above. Ironically, the company came through in Q4 beating the street on June 30, 2009.

The Current Situation

On February 24, 2010, H&R Block (HRB) reported their earnings which sank the stock price by more than 10%. How can this be when a great article was written on HRB on November 3, 2009? HRB shares should be approaching $40, not falling back below $20.

A Key Take Away

The key point here is not to say we are right or others are wrong. We simply felt that it was more luck than anything else that our article was published at or near the stocks' low. But remember our approach starts from the New Low Watch List which could explain a little about our "timing."

I have annotated the chart below to demonstrate what happened after our initial research recommendation of H&R Block (HRB). It's true that many people said we issued a sell recommendation too soon and missed out on the big upside (60%.) But one does not know that until after the fact. It took 242 days or nearly 8 months to accumulate a gain of 60%. But it only took 42 days or little over one month to wipe out half of that gain.

The current price of $17.20 is still above our sell recommendation. However, investors who are unwilling to accept the reality of gains (selling at higher prices) have to live with the reality of less gains or even losses. We are willing to accept any gain even if it is 16% of the 60% rise.

Going back to our initial question, how is it possible that a great stock like H&R Block (HRB) can be down/up so much? To which we answer, "we don't know." One person cannot justify the price rise or fall. Investors should be focused on the risk/reward of an investment opportunity rather than the reasons why. Of course, we only ignore the reason why with companies that have a proven track record of dividend increases.

During May 2009, the news and outlook for HRB was at its bleakest. However, bad news wouldn't likely move the stock down much further. But a glimmer of hope will shoot the stock up. The opposite occurred in early 2010. All the good news was baked in already. Any good news would no longer boost the price much higher, but a slight change in sentiment will crater the stock.

- Art

{kind=link}

{kind=link}