{kind=link}

{kind=link}

{kind=link}

- Japan

- Market Indicator

- Price Momentum Indicators

- Richard Russell

- Silver

- Speed Resistance Lines

- U.S. Dividend Watch List

Category Archives: Dow Fair Value

Dow Jones Downside Targets

Below are the downside targets for the Dow Jones Industrial Average applying Dow’s Theory and the Dow Jones Transportation Average applying Edson Gould’s Speed Resistance Lines.

Posted in 50% principle, Dow Fair Value, Dow Industrials, Dow Transports, downside

Tagged members

Dow Theory: Did Microsoft Overpay for LinkedIn?

The question has come up about whether or not Microsoft (MSFT) has overpaid for LinkedIn (LNKD). We’re going to apply Dow Theory to determine what would have been considered the fair value for LNKD based on the stock price. Next, we're going to see how much or how little MSFT paid for LNKD.

First, we need to establish what Dow Theory considers the fair value. According to S.A. Nelson, fair value is determined when…

"...stocks have recovered after artificial depression and relapsed after artificial advances to the middle point which represented value as it was understood by those who bought or held as investors."

The idea of “…bought or held as investors…” is very important as it reflects individual (or institutional) money that has decided to buy a stock with the expectation of holding for an extended period of time, usually 5 years or more.

Artificial Advance and Depression

When looking at the price movement of LinkedIn, it is easy to identify the artificial advances and depressions. However, to determine the fair value, a price which long-term holders of the stock have, on average, acquired the stock, we look to the middle point.

In order to determine the middle point (fair value), based on Dow Theory, we look at the previous major advance from the low to the high in the stock price. The previous low was $59.07 and the previous high was $276.18. The middle point (also know as the 50% principle) is $167.63.

LinkedIn Fair Value

If fair value for LinkedIn was actually $167.63 and Microsoft agrees to pay $196 per share, that would suggest a premium of 16.92%. How does this crude methodology stack up against institutional analyst assessments of fair value for LNKD? This from Morningstar.com:

“LinkedIn posted a better-than-expected start to 2016 as the firm beat both consensus estimates and management guidance for revenue and EBITDA, with strong performance across all three segments. We reaffirm the company's wide moat rating and our fair value estimate of $155. With shares trading just inside three-star territory in after-market trading, we would wait for a larger margin of safety before investing (source: Macker, Neil. “LinkedIn Starts 2016 By Beating Expectations, Management Remains Focused on Engagement”. Morningstar.com. 4/29/2016. accessed 6/14/2016.).”

Morningstar had $155 while Dow Theory assessed a $167.63 fair value. Although the Dow Theory method seems arbitrary, it is based in sound reasoning which we have covered before on the topic of the 50% Principle.

So, the question becomes not “did Microsoft overpay for LinkedIn?” instead it should be viewed by “how much did Microsoft overpay for LinkedIn?”. Based on Dow Theory, Microsoft didn’t pay much more than the company would have been worth to long term holders of the stock, in this case a premium of only 16.92%.

Posted in 50% principle, Dow Fair Value, LNKD, MSFT, values

Dow Theory: The 50% Principle

The following from Richard Russell’s Dow Theory Letters is what we believe to be one of the most valuable examples of Charles Dow’s 50% Principle in action.

“I am publishing this arithmetic chart of the D-J Industrials (high and low monthly) from M.C. Honey, Salisbury, Md. 21801. I am using an arithmetic chart because I want to show distance or ground covered by the Dow, not percentages.

“The 50% Principle states the following: After an extended advance, the termination point of the ensuing correction should be watched carefully. If the correction can halt while retaining 50% or more of the previous advance, it is a positive indication, and there is a good chance that movement will rally to test the area of the high again. Conversely, if the correction wipes out more than 50% of the previous extended advance, it is a negative indication, and there is a good chance that the movement will continue down, ultimately testing the area from which the entire advance started.

“It should be remembered that this is a theory, and although it has worked many times in the past there is nothing immutable about this theory (or observation, if you wish to call it that). Second, the 50% Principle should not be applied to short-term movements; it should only be applied to major movements lasting six months to a year or many years.

“There are two important applications of the 50% Principle which may be coming into prominence. First, referring to the chart, note that the Dow has broken the long-term trendline connecting the 1953 and 1962 bottoms. This is obviously a bearish indication, suggesting a reversal of the entire rising trend since 1949. The fact that this occurred within the framework of a primary bear markets makes the penetration of the trendline doubly significant. I do not believe, in other words, that this was a “false” penetration.

“If we measure advance, in the 1962 low of 535.76 on the Dow to the final 1966 peak of 995.15, we note that the movement carried 460 points. The halfway point of the 1962 to 1966 rise was thus 765. This means that during the 1966 and again during the most recent decline the Dow decisively broke the 50% level. The implication under the 50% Principle is that the Dow will probably test the area from which the movement began, or the 1962 area of 535. Whether this will happen remains to be seen, but at any rate that is the implication of the 50% Principle.

“The second important consideration is that the entire primary bull market covered a distance of 834 point; from the 161.60 of 1949 to 995.15 of 1966. The halfway point of the whole bull market rise is thus 578. I feel that if the Dow breaks to lower levels, it will be important to see what happens if and when 578 is approached.

“If a bottom can be formed at or above 578, particularly during a period which shows third phase characteristics, it will be a positive sign. Conversely, if 578 is decisively penetrated, I would take it as a most bearish and tragic sign. If 578 is broken decisively on the downside, my guess is that the final bottom of the bear market will arrive at an area far lower than anyone now thinks possible. (source: Russell, Richard. Dow Theory Letters. May 1, 1970. Page 3. www.dowtheoryletters.com)”

After the May 1, 1970 article by Richard Russell, the Dow Industrials had the following performance:

On December 6, 1974, the Dow Jones Industrial Average closed at 577.60. After this point, the Dow Industrials never closed lower. In the January 2, 1975 issue of the Dow Theory Letters, Russell said the following:

“Unless both Averages now break to new lows (Industrials below 577.60, Transports below 125.93) history will record October 3 as the bottom for the bear market (although December 6 will stand as the low day for the D-J Industrial Average alone).”

The 50% Principle is a necessary tool for all investors to gauge how much a decline is expected to run it’s course in the worst case scenario. A conservative investor should make use of the 50% Principle as a means of determining downside risk. With this in mind, the expectation is that at some point the stock (or index) will decline by nearly –50%. The 50% Principle sets the framework for how to interpret the price action from almost any prior peak.

In a roundabout way, even Charlie Munger, Warren Buffett’s long-time investment partner, considers the prospect of a decline by –50% in the following commentary:

“I think you can argue that if you’re not willing to react with equanimity to a market price decline of 50% two or three times a century you’re not fit to be a common shareholder and you deserve the mediocre result you’re going to get, compared to the people who do have the temperament who can be more philosophical about these market fluctuations.”

The 50% Principle Today

Below is the current 50% Principle for the Dow Jones Industrials Average.

While falling to 11,561.85 isn’t required, it doesn’t hurt to have a sense of the downside risk. Additionally, as the Dow goes higher, the level for the 50% Principle will increase. A retest of the ascending trendline should be expected at minimum.

Posted in 50% principle, Dow Fair Value

Dow Theory on Marvell Technology Buyout Rumors

Today the price of Marvell Technology increased +8.49% after news of KKR & Co. having acquired 5% of the chipmaker. According to Bloomberg News:

“KKR & Co. (KKR) has acquired almost 5 percent of computer chipmaker Marvell Technology Group Ltd. (MRVL), two people with knowledge of the matter said.

KKR sees the Hamilton, Bermuda-based company as undervalued and has discussed its holding with the company’s co-founders, Chief Executive Officer Sehat Sutardja and his brother Pantas, said one person, who asked not to be identified as the information is private. One scenario New York-based KKR is considering is a leveraged buyout of Marvell, though no such deal is imminent, the person said (source link).”

On our Nasdaq 100 watchlist dated June 20, 2012, we had the following to say about Marvell Technology (found here):

“Dow Theory suggests that the following are the downside targets for Marvell:

So far, Marvell has fallen within 6% of the $10.61 target, however, it has not breached that point thus far. We’d be buyers of the stock at $8.25 with little regard for downside risk at that point in time.”

Since June 20, 2012, Marvell has had the following price performance:

If measured by the very first day that Marvell fell below $8.25, the stock has increased +66.18% in just over one year ($7.57-$13.03). However, if Marvell were measured based on the price before the announcement of KKR’s interest in the stock, the increase in the stock has been +45.57%.

From our perspective, considering Marvell undervalued after a +45% run up in the price is a stretch. However, we suspect that KKR will try to squeeze out as much of this stock as possible. Charles H. Dow, co-founder of the Wall Street Journal, has the following to say on this particular topic:

“It is a matter of comparative indifference with a large operator whether the stock which he is handling is a point or two higher or lower. The thing which is important is whether the public follows up the advances so that he can sell (Dow, Charles H. Review and Outlook. Wall Street Journal. June 29, 1899.)”

In this case, the large operator is KKR & Co. Their goal is to see that Marvell rises as much as possible after they have taken a sizable position. One method to do this is to announce, through major channels of communication with unnamed sources, that they have taken a sizable position. What should happen next is continued speculation of whether or not Marvell is acquired by a competitor or another private equity firm, ultimately pushing the stock price higher. Unfortunately, those relying on such information may be caught holding the bag if all the rumors are proven to be just that.

It is Dow Theory that has pointed us in the direction of when to look to acquire or accumulate stocks and it is also Dow’s theory that suggests when to be cautious and possibly sell. For now, Dow Theory indicates that the fair value of Marvell is $14.58. Exceeding the fair value target offers up significant opportunity. Remember, a large operator like KKR isn’t aiming for a “point or two higher.” If the rumors are true, KKR probably has their sights set on $22 or above. However, any price above $14.58 should be considered speculation, at best.

“Affairs are easier of entrance than of exit; and it is but common prudence to see our way out before we venture in.” –Aesop

Comments Off on Dow Theory on Marvell Technology Buyout Rumors

Posted in Dow Fair Value, Dow Theory, fair profit, KKR, MRVL

Investing in Foreign & Emerging Stock Markets

Subscriber R.G. asks:

“If emerging markets possess such a gambit due to their lack of similar history in the past how can we analyze the markets in order to capitalize on their surges of demand which quickly taper[s] off?”

Our general view on foreign and emerging markets is similar to that of Warren Buffett’s when he said:

“'If I can't make money in the $4 trillion US market, I shouldn't be in this business. I get $150 million earnings pass-through from the operations of Gillette and Coca-Cola. That's my international portfolio’ (source: Ellis, Charles D. Wall Street People. page 56. link here.)”

There seems to be little need to invest in foreign or emerging markets. However, if there is a desire to invest in foreign markets then Dow Theory provides a reasonable template for how to approach investing in such a market. In a section titled “Dow's Theory True of Any Stock Market,” William Peter Hamilton says the following:

“The law which governs the movement of the stock market, formulated here, would be equally true of the London Stock Exchange, the Paris Bourse or even the Berlin Boerse. But we may go further. The principles underlying that law would be true if those Stock Exchanges and ours were wiped out of existence. They would come into operation again, automatically and inevitably, with the re-establishment of a free market in securities in any great capital. So far as, I know, there has not been a record corresponding to the Dow-Jones averages kept by any of the London financial publications. But the stock market there would have the same quality of forecast which the New York market has if similar data were available. (source: Hamilton, William Peter. Stock Market Barometer. Harper & Brothers Publishers, New York. page 14. link here.)”

When we speak of Dow Theory, we are referring to the emphasis of values, fundamentals in relation to price as they pertain to individual stocks and the stock market. We are putting less emphasis on the strict technical analysis of the equivalent industrial and transportation indexes.

To be clear, because we live in the United States we emphasize investing in the U.S. However, according to Hamilton, it does not matter which country that you’re in, investors should embrace the comparative advantage of living in a country other than the United States and should become experts of value opportunities in that region.

Posted in Dow Fair Value, Dow Theory, Value Investing, values

Values According To S.A. Nelson

S.A. Nelson is credited with coining the term "Dow's Theory." In fact, Nelson tried to convince Charles Dow to write a book about his articles in the Wall Street Journal but did not succeed. After failing to get Dow to write a book, Nelson wrote his own based on Dow's writing. The book titled ABC of Stock Speculation neatly lays the groundwork for Dow's Theory to be recognized and interpreted throughout history.

In one excerpt from the book A Treasury of Wall Street Wisdom, Nelson says:

"...stocks have recovered after artificial depression and relapsed after artificial advances to the middle point which represented value as it was understood by those who bought or held as investors."

This means that if an index or stock that has fallen below the halfway point of the previous advance or risen above the halfway point of a previous decline, then the index/stock is either undervalued or overvalued. If the index/stock has fallen close to the prior level of where the advance started and the index/stock is still fundamentally sound then the index/stock could be considered extremely undervalued. Likewise, if the index/stock has risen far above the prior high then it is considered overvalued.

When I start to consider investing in an individual stock, I only want to know if the price of the stock has reached a new 1-year low. From this vantage point, I can determine if the stock is trading at an extreme relative to the halfway point of the previous advance and decline. Again, this approach can only work if the company is generally in fair condition. This means that earnings exist, the dividend payout ratio isn't too high and management has a track record of rewarding the shareholders and etc.

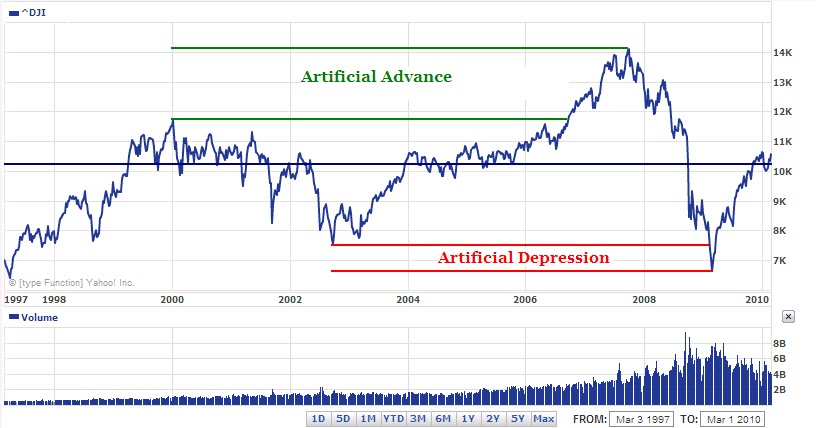

The halfway point of the previous advance or decline is the point at which "long-term" investors would consider the stock or index fairly valued. Traders can take advantage of this fact and use it to their benefit. In the chart below, I show the Dow Jones Industrial Average since 1997.

What is important to notice is that the artificial advance and artificial depression meet at the halfway point of 10,302.31 (dark blue horizontal line.) If drawn backwards to the point when the Dow first went above 10,000, we can see an enormous amount of time spent at or around 10,302.31 (as is currently the case.) This indicates that, for now, "long-term" investors fairly value the market at around the 10.3K level.

Take note of the fact that the Dow volume has fallen as the index has risen since the March 2009 bottom. This is in stark contrast to the bottom in 2003 which had volume more or less in a flat to higher range. As it stands, we have the upside limit to this market at the 11,722 level. Basically, we're still in a bull market rally, or cyclical bull, within the context of a secular bear market.

-Touc

This article was originally published in May 2009 on our former site Dividend Inc.

A Simple Way to Avoid Losing Money in Stocks

One of the easiest and most sure-fire ways to avoid losing money in stocks is to assume that every investment at some point will lose 50% or more. From this standpoint, all investments will be the most judicious and thoughtful. Transaction will not be entered into lightly.

Throughout my writing on the topic of investing, I have repeatedly stated that I always factor in losing 50% before buying a stock. Some readers have asked me, “Why in the world would you invest in something that you think could decline in value by 50%?” My response is always the same, if you haven’t accounted for the worst-case scenario then you aren’t really investing, instead you’re gambling.

I have found that by accounting for the downside risk of 50%, my mind is capable of assessing market declines with a more objective approach. Additionally, I am able to sleep soundly at night.

Below is a transcription of a BBC News interview of Charlie Munger who addresses the idea of accepting 50% loss in Berkshire Hathaway.

BBC News: How worried are you by the share price decline of Berkshire Hathaway?

Munger: Zero. This is the third time that Warren and I have seen our holdings in Berkshire go down, top tick to bottom tick, by 50%. I think it’s in the nature of long term shareholding with the normal vicissitudes and worldly outcomes and in markets, that the long term holder has his quoted value of his stock go down and then by say 50%. I think you can argue that if you’re not willing to react with equanimity to a market price decline of 50% two or three times a century you’re not fit to be a common shareholder and you deserve the mediocre result you’re going to get, compared to the people who do have the temperament who can be more philosophical about these market fluctuations.

It should be noticed that Munger mentions that he has experienced 3 instances of 50% declines in Berkshire Hathaway in the 42 years of its existence. This means that, on average, a portfolio is going to take a massive hit every 14 years or so. This assumes that you have the investment acumen of Warren Buffett and Charlie Munger. If you don’t have the investment savvy of Buffett and Munger, then the likelihood of losing 50% in your portfolio increases significantly.Now you know how easy it is to adhere to Warren Buffett’s rule number one, “don’t lose money.” After all, if you expect that your investments will lose 50% then you really start losing at 51%. Just be sure that you have the right strategy before you buy.

-

Before entering into a trade or investment, ask yourself if you’re willing to lose 50% or more.

Posted in 50% principle, Dow Fair Value, Uncategorized

Dow Theory on Fair Value

The purpose of this article is to demonstrate how Dow Theory approaches the question of the fair value of a stock. Most investors often hear of an analyst giving a fair value for a stock. Seldom is there ever a full description of the meaning of fair value or how exactly fair value is arrived at. Even when there is a description of how fair value is arrived at most investors have a hard time understanding what exactly it means if a stock they own goes from undervalued or overvalued to fair value.

Another name for fair value is intrinsic value. One source that we would derive our definition of intrinsic value is in Security Analysis by Graham and Dodd. According to a 1962 edition of Security Analysis:

“A general definition of intrinsic value would be ‘that value which is justified by the facts, e.g., assets, earnings, dividends, definite prospects, including the factor of management.’ The primary objective in using the adjective ‘intrinsic’ is to emphasize the distinction between value and current market price, but not to invest this ‘value’ with an aura of permanence. In truth, the computed intrinsic size is likely to change at least from year to year, as the various factors governing that value are modified. But in most cases intrinsic value changes less rapidly and drastically than market price and the investor usually has an opportunity to profit from any wide discrepancy between the current price and the intrinsic value as determined at the same time.

“The most important single factor determining a stock’s value is now held to be the indicated average future earning power, i.e., the estimated average earnings for a future span of years. Intrinsic value would then be found by first forecasting this earning power and then multiplying that prediction by an appropriate ‘capitalization factor.’”

Graham and Dodd. Security Analysis. McGraw-Hill. New York. 1962. Page 28.

The challenge with the definition of intrinsic value is the “facts” as described by Graham and Dodd. First, the valuing of assets could be done above or below their true worth. Second, earnings could be managed or manipulated in a fashion that is inconsistent with the company’s true health. Third, a company’s prospects are subject to vagaries in the market and therefore are not definite. Fourth, depending on the compensation method used for the company’s management, those in charge may act in a fashion that is counter to the continued growth of the company. The only certainty is the payment of dividends that have already taken place. In my experience observing stocks, I have seen the change in management, earnings, prospects and assets but never the change in ex post dividend payments.

Even within the definition of intrinsic value, Graham and Dodd submit to the fact that we cannot expect current conditions to exist into perpetuity. Additionally, the idea of forecasting into the future, “over a span of years,” a company’s earning potential seems to be more hopeful than anything else. The fair value of the company can decline with little more reason than a significant decline in stock price.

The spurious nature of intrinsic value can be demonstrated in what is known as an impairment charge. Recently there have been two Dividend Achievers that have had impairment charges which have significantly reduced the fair value of the company. In one instance, Supervalu (SVU) noted in their Form 10-Q filing that the “retail food operating loss for the third-quarter and year-to-date ended November 29, 2008 reflects the preliminary estimate of goodwill and asset impairment charges of $3,250,000 related to the write-down of goodwill and other intangible assets required by Statement of Financial Accounting Standards (SFAS) number 142.” What this means is that because the stock price fell so much in such a short period of time, the company was forced to adjust their fair value lower due to SFAS rule number 142.

In another example, Nacco Industries (NC) stated in their 4th quarter earnings call that, “during the quarter, the company wrote off the goodwill on its books. Because the company stock price at year end was significantly below the company’s books by tangible assets and its book value of equity, accounting rules effectively required the company taking non-cash write-off of goodwill and certain other intangible assets totaling $436 million or 431.6 million net of taxes of $4.1 million the company recorded those pretax charges as follows…” Again, this is an example of accounting rules (SFAS rule No. 142) determining the change in the value of the stock’s fair value.

Although these were “legitimate” changes to the fair value of the companies, one cannot overlook the fact that much of the fair value can be based on interpretation. Also, the timing of the changes can occur at times that are not consistent with the decline in earnings or future prospects. In the two prior examples these declines in fair value were based on the declines in stock price due to the market panic from 2007 to 2009.

Most fundamental analysis of stocks has been done based on the Graham and Dodd method which was codified in 1934 after the stock market crash from 1929 to 1933. Before 1929, there were other methods for determining a company’s fair value. One method that I have studied extensively is the Dow Theory method. Most followers of Dow Theory might not realize it but the “50% Principle,” as coined by George E. Schaefer but elaborated in great detail by Charles H. Dow, is the method for arriving at a stock’s “fair value.”

From a Dow Theory perspective, a company’s fair value is as simple to determine as the prior period of increase or decline in the stock price. However, understanding the nuances will allow for better interpretation of the meaning of fair value according to Dow Theory.

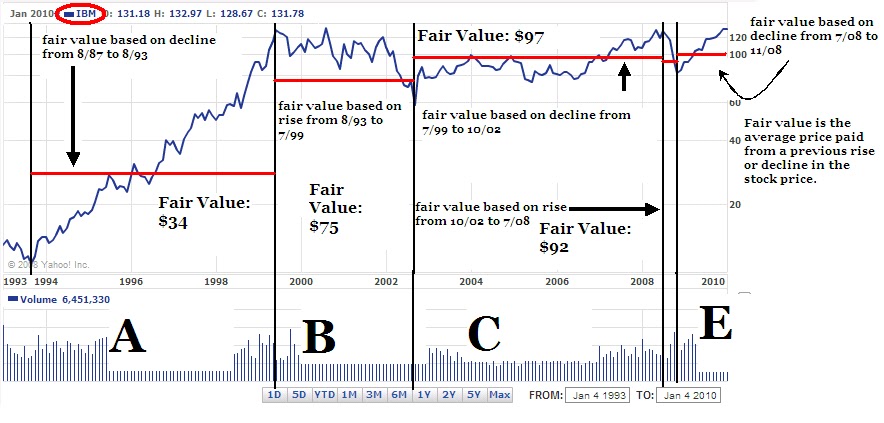

According to Dow Theory, fair value is arrived at based on one half the previous increase in the stock’s price or one half the previous decrease in the stock price. In the example above, I have selected IBM to show how fair value works according to Dow Theory.

In section A, I have indicated that the rise in 1993 to the peak in 1999 had an established fair value based on the prior decline from 1987 to 1993 (red line.) The prior declining period set fair value for IBM at $34. When IBM went from $10 up to $34 the company’s stock was considered at fair value. Any further increase in price was considered overvalued. Theoretically, any investor who bought the stock below $34 should accept that any further increase in price is icing on the cake.

Because the stock rose from $10 to $140 in the period from 1993 to 1999, a new fair value was established at $75. Section B carried the fair valuation of $75 indicating that anyone who bought the stock below $75 was getting a bargain.

In section C, I have indicated that the decline from 1999 to the trough in 2002 established a new fair value for the following increase at $97. In section C, from the 2002 low to the 2008 high, the fair value became $92. In section D, after the decline from July 2008 to November 2008 the new fair value became $100 in section E.

Each time a stock completes a major decline or increase, a new fair valuation can be established. For the cautious investor, the fair value for the next increase is derived from the previous decline and the increase that preceded the previous decline. This establishes a range that an investor would determine where a stock is fairly valued. A real-time fair value can be determined based on the most recent price trend however, an investor has to accept that, without a turn in the price (confirmation), the position is at significant risk. Below is an attempt to demonstrate how the process works.

In July 2008, an analyst issued a strong buy report on Lowe’s (LOW) when the stock was trading at $18.90. At the time, the analyst indicated Lowe’s had a fair valuation of $32.27 using an assortment of Graham and Dodd methods. However, if using the Dow Theory method for determining fair valuation, an investor would have arrived at a fair value of $26.92.

Old high of $34.93 set on 2/20/07

[($34.93-$18.90)/2]+$18.90=$26.92

Subsequent to the report that was issued at $18.90, LOW closed at $27.36 on September 8, 2008 and then traded down from that point until it rested at the $13 level in March of 2009. Using the Dow Theory method for fair valuation, an investor would have sold the stock on the approach to $26.92 and then waited to see what would have developed from there. My personal modification to this method is to move on to a different stock altogether.

Unfortunately, a person who followed the analyst recommendation of expecting the stock to go to $32.27, or fair valuation, would have held on regardless of the stock never getting to $32 and instead declining back to $18.90 and below.

Now with LOW at $13, the new fair value, according to Dow Theory, based on the old high of $34.93, is $23.97. Well, from the $13 level, LOW traded up to $24.17 and has since reversed to the downside at the current price of $23.13. Again, the investor following the Dow Theory method would have sold the stock as it approached the $23.97 level.

Anyone who had based their purchase of LOW on July 2008 using the analyst’s future fair value of $32 would have not seen the price come close to predicted fair value.

While not infallible, the Dow Theory method addresses the most primary elements seen by all investors, the price movement. Although background in Graham and Dodd never hurt anyone, fundamentals are, at times, a distraction from what the most uninitiated gambler can see without having to crack open a single investment report. Additionally, an equal number of investors and speculators are on either side of the fair value range. This gives incentive to either buy, hold or sell the stock based on crossing the fair value plane.

Some would ascribe the Dow Theory 50% principle to the use of Fibonacci counts however, R.N. Elliot’s popularization of the application of Fibonacci’s to stock prices didn’t catch on until long after the establishment of Dow Theory. The use of Dow’s Theory in determining fair value gives investors the opportunity to see exactly how much the market discounts everything. It is clear that buying and selling a stock in such a short period of time is considered diametrically opposed to the Graham and Dodd method. However, it would benefit all who wish to obtain a reasonable approximation of fair value to consider the Dow Theory approach. -Touc

- Moves to the downside project fair values for the upside. Moves to the upside project fair value for the downside.

Posted in Dow Fair Value, Dow's Value Theory