Dow Theory Letters issue 742 was published on November 1, 1978. At the time, the Dow Jones Industrial Average indicated was at the 806.05 level. In this issue, Richard Russell discusses several topics that are very important to every Dow Theorist.

First, Russell states that:

“…history shows that when bull (or bear) markets really begin, Dow Theory signals are generally greeted with derision, skepticism, and scorn-rather than wholesale agreement!” page 1

This comment is in response to the Dow Theory bull market signal that was given on August 2, 1978. In this case, Russell felt there wasn’t enough skepticism by market participants to warrant a need to trust the signal. I’m guessing that after 12 years of a secular bear market any good news about the market would appeal to the glass half-full crowd.

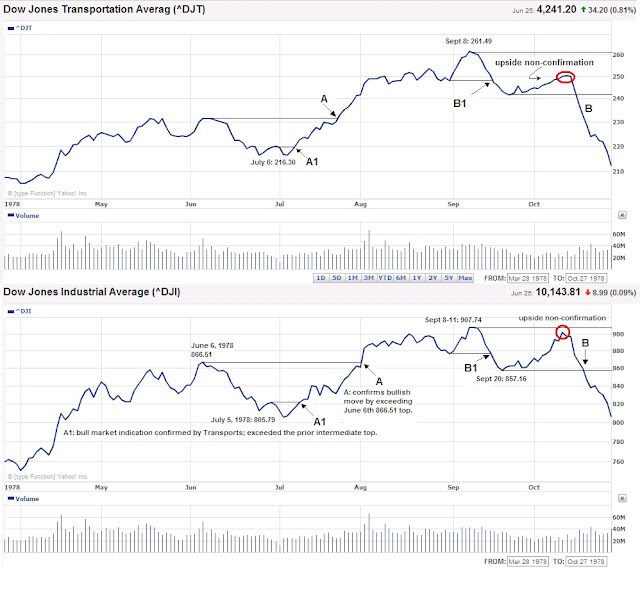

Letter 742 also has a chart (located here) of the Dow Jones Industrials, Transports, Utility Averages and NYSE volume. Upon closer inspection of the chart below, ranging from March 28, 1978 to October 27, 1978, you can find two confirmations of a bull market and one confirmed bear market indication as part of Dow Theory.

According to Russell, point A (August 2nd), on the Dow Industrials, was a false secondary peak or bull market indication. However, it should be noted that when the Industrials went above the June 29th peak of 821.64 (point A1) on July 21st it was a clear indication that the index was going to retest the previous high at point A.

After the bull market move upward a bear market indication was given when the Industrials and Transports fell below point B1 that corresponded to the August 31st low of 876.82 and 248.78 respectively. A bull market non-confirmation was indicated (red circles) in the fact that neither index could exceed the high of September 8, 1978.

Let’s do the math for a moment, point A1 gave a buy signal plus point A’s confirmation of the buy signal equaled a 9.62% rise by the time the market gave the bull market non-confirmation at Dow Industrials 900. The same timing applied to the Dow Transports would have equaled a gain of 13.64%. To my mind, this was in line with our view that any return close to 10% in less than a year is an acceptable amount to trigger a sell of any stock.

Russell also repeats a common attribute that he seeks in the market before considering going “all in.” Russell says:

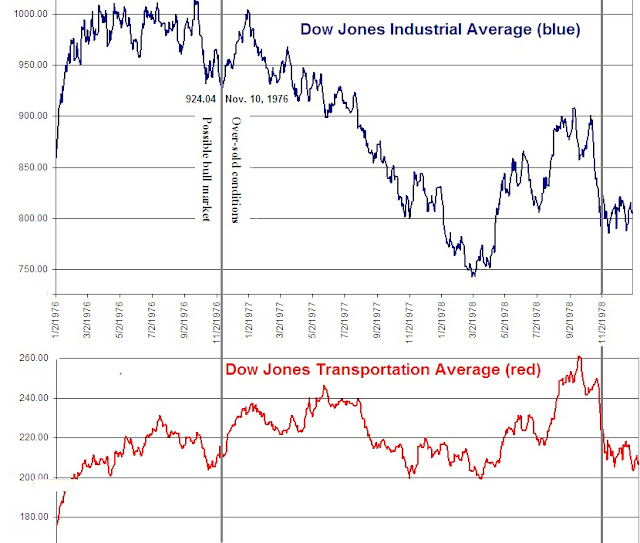

“I noted that every bull market in history had started from an over-sold base, but that this market had not seen a over-sold condition since late-1976.” Page 1.

In this remark, I have two thoughts that immediately come to mind which is reflected in the chart below. The first is that even after the 1974 bottom there was another time (1976) that was “most ideal” to buy stocks at over-sold levels, according to Russell. However, even though late-1976 was experiencing oversold conditions, it certainly didn’t mean that further declines were out of the question. After the ’76 bottom, the Dow Industrials had a short rally and then fell as low as 742.12, a decline of 19.69% from the 1976 lows, by February 28, 1978. Finally, the view that an over-sold base is a condition necessary for a bull market may not be accurate.

On page 2 Russell said:

“Right now, I want all my subscribers to stay out as per my instructions in Letter after Letter.”

This suggests that after the January 1975 buy signal given by Russell, it was very difficult to keep a long-term position even though it was the absolute best time to “buy and hold” stocks.

“The violence and rapidity of this smash has few precedents in stock market history.” Page 2.

When calculated to the November 14, 1978 low, the decline from September 8, 1978 equaled a drop of 13.5%. To me this doesn’t seem like all the much of a decline.

“Somewhere in the period ahead, we are going to see the real ‘third phase bear market action’ in the Dow and most other stocks. True, during 1973-1974 the majority of stocks were pulverized in a slide that was comparable to 1929-32 in many ways. But the Dow lost less than 50% of its value at that time. My guess is that before the third or final phase of this bear market is over, we are going to see the Dow at drastic new lows, we’re going to see dividends cut across the board, we’re going to see very high interest rates, and we’re going to see something that this generation has never seen before-wholesale liquidation of debt in all sections of the economy, private, corporate and perhaps even government.” Page 2

“Each time it looks as if the ‘plug is going to be pulled,’ the bear market (with the help of huge infusions of monetary inflation from the Fed) pulls itself out of the hole.” Page 2

Russell was waiting for the third phase of the bear market. According to Russell, the Fed was holding the market up with the trade-off being higher inflation. My thinking is that a crash didn’t occur simply because the Fed was willing to accept higher inflation as a substitute for a crash. In addition, if the markets were to get a crash and record inflation at the same time it would be exceptional situation. The third phase decline that Russell expected never seemed to materialize on the scale of 1973-74 or greater.

Other Notes in Letter 742:

- E. George Schaefer’s investment performance from 1949 to 1966.

- James Dines book the “Invisible Crash”

- MC Horsey’s chart of an inflation adjusted Dow since 1960

- Benjamin and Herbert Stein’s book “On the Brink” with reference to, of all things, the Chinese cornering the gold market

More:

{kind=link}