Reader Kerry Comments:

“I’d like to pick up on the problem that untrusting investor has identified ‘The problem is that we have never seen one yet that has much accuracy or predictive ability to any substantive degree or within any reasonable time frame. As such, it becomes a ‘big gamble’ to take action on the predictions of any such cycle models or theories.’

“I like cycles myself, but I struggled with cycles that appeared great but then tended to be slightly off when forecasting the future, and therefore are difficult to use in trading. This led me to conduct my own research that has culminated in my own cycle work and the discovery of a 2.2/4.4 year cycle. I am of the opinion that the secular bear is about to strike back in the second half of 2013 as the 17.6 year stock market cycle continues until 2018, when the next great bull market will properly begin.”

Our Response:

Implicit in the discussion of cycles (observations of the past) is the eventual application of the analysis for the future. Unfortunately, some who do the best research on the study of cycles have the worst record of application. Our view is that we’ll be wrong about the actual cycle range and the application of the timing. Therefore, we are never disappointed about the outcome.

However, as students of the market we are constantly working to find quality research on the topic. Already we know that Charles Dow’s work on stock market cycles is useful when applied with skepticism and moderation.

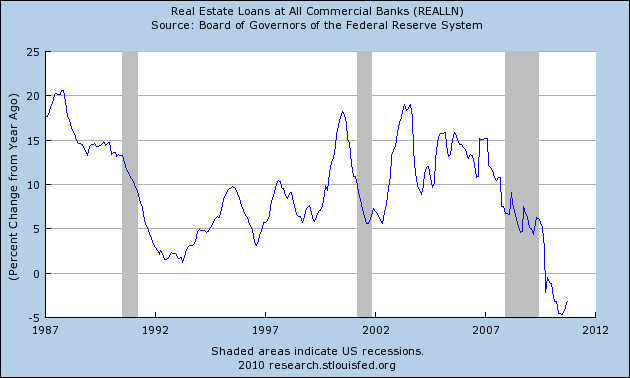

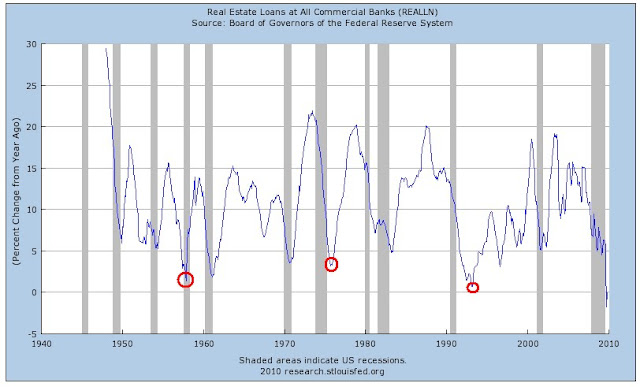

As an example, based on the Wenzlick model for when real estate would bottom (18.3 years) it suggested that the low would be in 2009. In our January 2010 article titled “Real Estate: The Bottom is Calling” we said the following (found here):

“…tendency has been to include the years 2008 and 2010 just to play it safe.”

We understand that the markers for a bottom or top are like sand dunes in a desert, they are constantly on the move. This does not negate the cyclical nature of market moves, it just means that flexibility is required when thinking on the topic of cycles.

We followed up the January 2010 article with what we believed was the definitive call in the real estate bottom based on the work of Wenzlick. In a December 2010 article titled “Real Estate: The Verdict is In” (found here) we felt the title said it all.

Naturally, we could have been completely wrong and in select markets, a bottom may not be in at all. However, we’re trying to think in terms of the broader context. Based on the metrics that we tracked, real estate did hit bottom on or fairly close to the December 2010 low as highlighted in our follow-up article titled “Real Estate: A Sustainable Rise” (found here).

Within the general context of “being accurate” on our call of real estate based on the cycle work of Wenzlick, there are a couple of MAJOR ASPECTS THAT WE DID NOT GET RIGHT and that is the recommendation and investment in homebuilder stocks and the purchase of the home in our specific county.

First, we did not recommend homebuilder stocks because we simply didn’t think of it. That was a huge missed opportunity as shown in the chart below of the SPDR S&P Homebuilders ETF (XHB).

Second, our purchase of a home in September 2009 was not at the low point, for our region of the country, as real estate prices had bottomed in January 2009. By the time of the 2009 purchase, median prices for our county had increased by +40% as seen in the chart below (www.car.org).

Also, as seen below, existing home sales for our county bottomed a year after the home purchase.

However, the overall point is that we're closer to the low in the respective cycles rather than near the peaks in the cycle with out investments and purchases. Additionally, we’re taking the lessons for the current cycle and hoping to apply it to the next cycle move.

We also have cycle targets for gold and interest rates which have been fairly accurate. Do we go “all in” on the cycle turns? No. However, we do factor in the chance that the change in the cycle could exert its force on our best intentions.

Again, the emphasis should always be on skepticism and moderation when attempting to apply cycles for predictions of the future. With this in mind, a good analyst will hedge their commentary on cycles and allow for a wide margin of error. After all, we’re all students of the market (real estate, jobs, stocks, cars, groceries etc.) and therefore open to changing conditions.

As mentioned earlier, we’re always factoring the downside risks and acting accordingly (most of the time, except when our subscriber SD pointed out the awesome buying opportunity on DELL from our own watch list at the low…Great call SD!).

If we haven't hit bottom yet it means that within the year 2010 we will have to go below the previous low prices of 2009. Such an occurrence would be a complete disaster for the financial markets. I am hopeful that the real estate market doesn't further devolve. However, the concern does rest in the back of my mind.

If we haven't hit bottom yet it means that within the year 2010 we will have to go below the previous low prices of 2009. Such an occurrence would be a complete disaster for the financial markets. I am hopeful that the real estate market doesn't further devolve. However, the concern does rest in the back of my mind.