Reference:

- “Considering the Downside Prospects for Apple”. April 14, 2012.

- “Review: Apple’s Altimeter”. July 17, 2013.

Reference:

Posted in AAPL, Altimeter, Apple Computer, Edson Gould

Price change since August 1, 2014 recommendation of WFM:

We said the following at the time:

“Investors interested in WFM should consider a 3 step purchase plan with the first purchase at the current price with additional investments at $30 and at $24 or below. It appears that WFM has considerable price support at the $24 level.”

Gould’s Speed Resistance Lines

Posted in Altimeter, downside, Edson Gould, speed resistance line, SRL, WFM, WFMI

According to Yahoo!Finance, “Dover Corporation manufactures and sells a range of equipment and components, specialty systems, and support services in the United States. The company operates in four segments: Energy, Engineered Systems, Fluids, and Refrigeration & Food Equipment. The Energy segment provides solutions and services for the production and processing of oil, natural gas liquids, and gas to drilling and production, bearings and compression, and automation end markets.”

The price of Dover Corp. (DOV) has declined by –32.46% since the early July 2014 peak. Looking at the stock, it appears that the downward spiral is locked in. The following are some thoughts about the stock.

Posted in Altimeter, Charles H. Dow, DOV, Dover, Dow Theory, Edson Gould, Quick Take

In April 2012, we published an article titled, “What Does Warren Buffett See In IBM?” At the time we concluded the article with the following thought:

“…just imagine what IBM will look like after falling to a 52-week low.”

A reader of our article took exception to the idea of IBM declining in price with the remark:

“I have no idea why you think you could buy IBM on a 52 week low. There is nothing fundamental about the company that would lead one to think that might happen. IBM is a difficult company to short because people who own it primarily intend to hold it for a longer term, do not trade on margin, and do not sell their shares based on fear (Momintn. What Does Warren Buffett See in IBM? April 19, 2015. link.).”

Since our article, IBM has declined from $207 to $161 with upside movement being limited to $213.

In spite of the price decline of nearly –22% since 2012, IBM has increased the dividend by +53%. This has resulted in a situation where the price of IBM has becomes very compelling from a value perspective. As indicated in our original article on IBM, the growth of the dividend has become an overpowering force which is creating a stock that could eclipse all expectation for long-term investors. This leaves aside the topic of IBM share repurchases which Warren Buffett discussed in his 2011 shareholder letter.

Our premise of IBM’s valuation is narrowly perched on the work of Edson Gould’s Altimeter. Below is an update of Gould’s Altimeter since our April 2012 article.

According to Gould’s Altimeter, IBM is now undervalued below the levels of the 2008 low. We think that a value investor would have fun pouring over the data to determine the actual value of IBM. Gould’s Speed Resistance Lines [SRL] indicate that the conservative downside target for IBM is $130. However, we think a process of accumulation at the current price, and below, is a prudent long-term strategy.

Posted in Altimeter, Edson Gould, IBM, SRL

We’re always hopeful and expectant about the future prospects of any investment that we make. However, that doesn’t mean that we’re going to ignore the most pressing matter when investing which is assessing the downside risk. Below is the downside risk assessment for Hospitality Properties Trust (HPT) based on the work of Edson Gould.

The first tool of Gould is the Altimeter. This assesses a stock based on the stock price relative to the dividend that is paid. In this case, HPT has come off of a recent high near 70. This high matched the high of late 2006, the subsequent decline brought the stock price down nearly –80%. We don’t think that it is realistic to believe that HPT will decline as in the period from 2006 to 2008. However, we’ve outlined in red a low that we feel is reasonable if a decline were to take place. This low is at the $21 level where there appears to be a common retracement point.

If worse comes to worse, HPT could decline to point A or $13.00. If a repeat of the housing crisis were to take place then HPT could decline as low as point B or $4.67.

The other tool that Gould used was the Speed Resistance Line [SRL]. The SRL is ideal for stocks that increase significantly out of proportion to the general stock market. As HPT has increased nearly twice that of the S&P 500, we feel that the SRL is the most appropriate assessment for downside risk.

In this case, the SRL indicates that the conservative downside target is $26.22. In the previous decline of 2006 to 2008, HPT declined to the previous low set in 1999 at slightly below $5.00. However, as we mentioned before, we don’t think that this time is anything like the rise and fall of the housing bubble. Therefore, we’re looking for HPT to successfully breach the $26.22 level and retrace to the $18.86 level before a possible rebound. Our experience has been for HPT to adhere to the ascending lines for most stocks that we have covered in the past.

Who is Edson Gould?

"Edson Gould spent over 60 years working in and studying financial markets. Gould studied the arts at Princeton, engineering at Lehigh (from where he graduated in 1922), and finance at New York University. In 1922, after working for a short time at Western Electric, he joined Moody's Investor Service as an analyst and later was editor of Moody's Stock Survey, Bond Survey, and Advisory Reports. In 1948, he began at Arthur Wiesenberger & Company, where he developed and edited the well-known Wiesenberger Investment Report and became a senior partner. He also was Research Director at E. B. Smith (which later became Smith Barney), and worked for Nuveen."

(source: Market Technicians Association. Gould, Edson Beers, Knowledge Base. Accessed April 26, 2012. link MTA reference.)

"Market technician Edson Gould always laughed at the idea of having a significant influence on the stock market, but his predictions were the most precise around. He pinpointed major bull markets and prophesied bottom-out markets as if he had his own peephole into the future. But in place of a crystal ball and wacky off-the-cuff schemes, his were smart, intensely researched and time-tested theories that made him a legend in the investment community."

(source: Fisher, Kenneth L.. 100 Minds That Made the Market. Business Classics, Woodside, CA. 1993. page 320.)

Posted in Altimeter, Edson Gould, HPT, speed resistance line, SRL

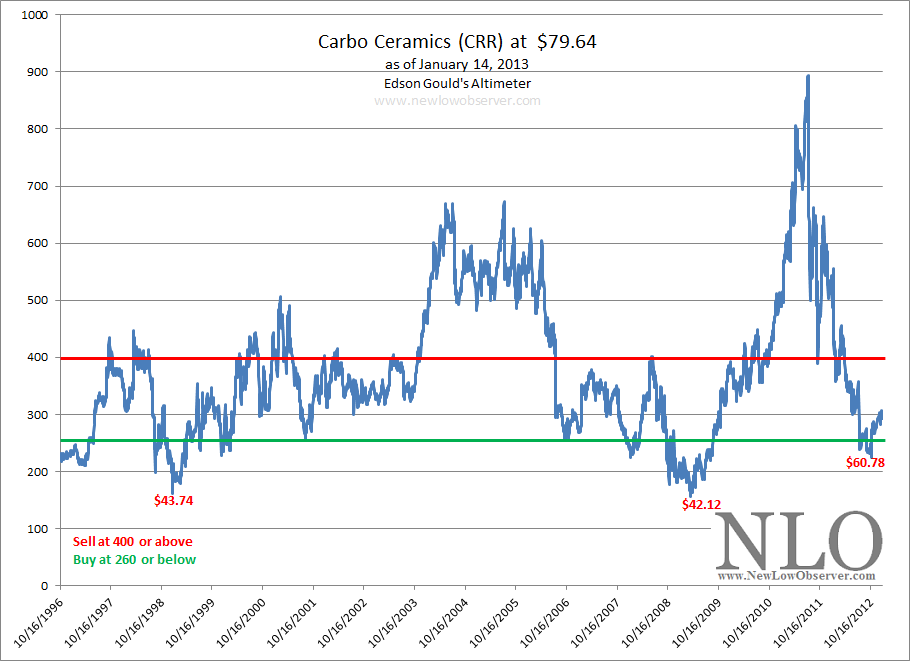

Review

On August 6, 2012, we purchased Carbo Ceramics with the following rationale:

“Carbo Ceramics (CRR) has been mentioned by us on several occasions. CRR first appeared on our February 10, 2012 U.S. Dividend Watch List (found here) and was trading at $85.94. An Altimeter was run on CRR which indicated that the stock would be undervalued at $62.40 (found here). However, as CRR has experienced a dividend increase of 12.5% since our May 28, 2012 Altimeter, the stock is now considered undervalued at $70. While we do expect approximately 20% downside risk from the current price, we are comfortable with adding to our position when such a decline takes place.”

As it appeared that Carbo was undervalued between $62.40 and $70, we used 5% of our portfolio to purchase the stock. After August 6, 2012, Carbo Ceramics fell as low as $63.03 and increased as much as $156.

Update

Below are the updated numbers for Carbo Ceramics after the decline from the most recent peak of $156. We will cover both aspects of CRR based on Gould’s Altimeter and Speed Resistance Lines. First, the qualitative review based on the Altimeter.

“The valuation problem is far from academic: In recent years, some huge-scale frauds and near-frauds have been facilitated by derivatives trades. In the energy and electric utility sectors, for example, companies used derivatives and trading activities to report great ‘earnings’ – until the roof fell in when they actually tried to convert the derivatives-related receivables on their balance sheets into cash. ‘Mark-to-market’ then turned out to be truly ‘mark-to-myth.’”

Buffett, Warren. Berkshire Hathaway. 2002 Letter to Shareholders. February 21, 2003.

In our May 6, 2012 posting on Berkshire Hathaway (BRK-A) titled “Should Berkshire Hathaway Be Trading at 1995 Prices?”, we gave price projections based on Edson Gould’s Altimeter using very conservative estimates if BRK-A paid a dividend. As we’ve managed to achieve the middle of the three upside targets set down in our 2012 article, we’re going to list the price that we think BRK-A would be considered undervalued for each of the next 10 years.

Posted in Altimeter, BRK-A, Charlie Munger, Edson Gould, Warren Buffett

Tagged members

On May 6, 2012, we proposed that Berkshire Hathaway (BRK-A) was trading at a price that was well below its true value. At the time, BRK-A was trading at $164,990 per share. However, we proposed that Berkshire Hathaway should have been selling at much higher prices with upside targets of $175k, $197k and $219k in a 2-3 year timeframe. As BRK-A sits within 1% of our mid-range target of $197,190 after two years, we believe it is time to reassess where Berkshire Hathaway sits within the context of Edson Gould’s Altimeter.

Posted in Altimeter, BRK-A, Edson Gould, Warren Buffett

As the Dow Industrials meander near all-time highs, it is necessary to review Edson Gould’s Altimeter for the index.

Posted in Altimeter, Dow Industrials, Dow Theory, Edson Gould, Geraldine Weiss

Carbo Ceramics (CRR) was one of the companies that appeared at the top of our dividend watch list for many weeks beginning in February 2012. The watch list served as a beginning point for our research and we took a position in August (found here) at $65.02 (green arrow on chart below). Within three months, we saw shares of CRR rally to $74, a +13.8% gain. As such, we ‘hedged’ our position by selling the principal (found here) and let the profit run (red arrow on chart below).

Recent activity in Carbo Ceramics price suggests that, on a technical basis, the decline is over. Though a rally to its intraday peak of $180 is not expected, we believed there is a good opportunity for those interested in a short to medium-term speculative position in the stock.

In our view, the biggest bull case, on a technical basis, is that the 50-day moving average has crossed above the 150-day moving average creating what some call a "golden cross." We rely on the 150-day versus the more popular 200-day moving average for the fact that it is the road less traveled and provides an indication ahead of the crowd.

Currently, shares of Carbo Ceramics are trading just above the 50-day moving average, making this an ideal short-term transaction. For those who wish to trade this generally significant technical pattern, we’d consider selling if shares close below the 150-day moving average or if the stock gains +10% or more.

From a fundamental standpoint, Carbo Ceramics (CRR) provides long-term holders of the stock with the following attributes:

What Is the Downside Risk If I Want to Hold CRR for the Long-Term?

Dow Theory has the following downside targets for Carbo Ceramics:

Based on the work of Edson Gould, Carbo Ceramics has the following Altimeter:

Carbo Ceramics would have to fall to $70.20 in order to be considered a buy using the Altimeter above. However, as has been the case in the past, seldom does the Altimeter decline to the buy level and then immediately reverse to the upside. therefore we’d expect a push below the $70.20 level for good measure.

Edson Gould’s Speed Resistance Lines have $65 as the downside support level.

The most conservative of the three downside targets mentioned above is the Dow Theory level of $61. This seems be the most appropriate level to consider a first, or second, purchase if the desire is to hold Carbo Ceramics for the long-term.

Comments Off on Technical Review: Carbo Ceramics (CRR)

Posted in Altimeter, CRR, Dow Theory, downside, Edson Gould, SRL

We read a great article by Vince Martin titled “Procter & Gamble Is Severely Overvalued” (found here). Martin went through a detailed analysis of the reasons why Procter & Gamble (PG) should be considered an overvalued stock. Because Martin did not mention selling the stock (a cardinal sin of dividend investors), given such a strongly titled article, we thought we’d try to estimate what the downside risk for PG might be so that investors could prepare for when to buy the stock.

Keep in mind that as of October 12, 2012, Procter & Gamble (PG) has a price chart with the following activity since early 2007:

Overall, the price of PG has vacillated widely with a high of $74.67 and a low of $44.18. Dow Theory suggests that the midpoint of such a range is the dividing line between a stock that is bullish or bearish. In this case, the midpoint is $59.43. As can be seen by the rise from the 2009 low, PG has found significant support at or near the $59 level. This suggests that there is a bullish bias for this stock as accumulation seems to occur just below $60. Keep in mind that any significant decline below $59 is considered bearish and could be the beginning of a retest of the 2009 low.

Although the article noted above did not indicate that there was a specific downside target to “fair” valuation or undervaluation, we believe that such a point must exist. So far, Dow Theory and price activity since 2010 suggests that a fair or undervaluation sits around the $57-$59 level. However, when viewed from Edson Gould’s Altimeter, PG seems to be trading at the equivalent of 1991 prices as seen in the chart below:

Gould’s Altimeter indicates that based on the current dividend, provided there are no dividend increases going forward, PG is undervalued and has critical support at the $55 level. Any further increases in the dividend will only increase the undervaluation of the PG profile. For now, Edson Gould’s Altimeter confirms what Dow Theory seems to indicate and that is that at the $55-$59 range, Procter & Gamble should be aggressively accumulated.

Another area of concern is the dividend payout ratio. According to the article mentioned above:

“Assuming that 2013 dividends are paid at 60 cents quarterly -- a 6.7% raise, lower than any hike in the past decade -- the dividend will have risen 50 percent from 2008 to 2013, a period over which earnings are expected to rise just 14 percent. That is simply not sustainable, and as a result, in fiscal 2013, PG's payout ratio will almost definitely surpass 60 percent. In fact, on a free cash flow basis, PG's payout ratio has already passed that level, jumping from 58 percent in FY2011 to nearly 66 percent in FY2012.”

At some point, the dividend payout ratio can become the Achilles’ heel for PG if earnings aren’t sustainable. However, we believe that the earnings profile of PG will evolve and remain sustainable over time. In fact, while Value Line Investment Survey confirms Martin’s expectation for an annual decrease in earnings of -8% for 2013, PG is projected to increase their earnings by +53% in 2015-2017, bringing the fair value estimate of the stock to $97. This fair value estimate comes with a 100% “earnings predictability” rating from Value Line (dated 9/28/2012).

Obviously, anything can happen with a stock during such volatile times. However, we believe that Procter & Gamble, while not cheap, is a reasonable stock to accumulate if an investor is looking for a 4 to 6-year holding period. Aggressive accumulation of PG should take place if the stock declines to $59 and below.