I watch with glee as

Yahoo!Finance includes a price quote for gold in the Market Summary section on their home page. After all the financial turmoil that we've been through since the introduction of the internet, when did Yahoo!Finance realize that a gold quote was necessary? The obvious answer is, "When the public demands it."

Well, when the public finally demands the price quote of gold on their finance homepage, it is probably too late to participate in gold on a level that could be considered meaningful. After all, at nearly $1000 an ounce, there isn't going to be a stock split in the price of gold. Or is there? (I've been pondering this possibility lately) In any event, gold is fast becoming an expensive asset in a world full of correspondingly deflating alternative "assets." What to do? What to do? Get out there and do your research on silver!!! That's what you do!!!

I say do your research on silver because if I told you that, regardless of the Hunt Brothers cornering the silver market in the 70's, the price of silver always outpaces gold on a percentage basis by a ridiculous margin, you'd probably laugh in my face. But as you should know, silver is the "poor man's gold" and coincidentally, there are more "poor" men than rich men can afford to buy.

When I first bought gold and silver back in 1996 (in bulk and never purchased again), I knew that I was getting a bargain. When I exchanged 75% of my gold for silver in 2008, I knew I was committing highway robbery. I've always noted that "gold bugs" were blinded by the historical significance of the yellow metal, while at the same time claiming that they were investors who used gold as a form of insurance against government mismanagement of paper currency.

The real deal is in the price of silver. While gold has run up 259% since I purchased it, silver has gone up only 266% in the same period. This means that silver hasn't appreciated as much as it historically should relative to the price of gold. Which begs the question, what should we expect silver to do relative to gold? I have my own calculations for the future price of gold and silver. But more importantly, let's look at what history has to offer us.

I like chopping everything into halves. This means that if the Hunt Brothers' cornering of the silver market brought the price of silver to $50 then the real price probably should have been $25. From this vantage we now have to choose a starting point. Where did the price of silver start out?

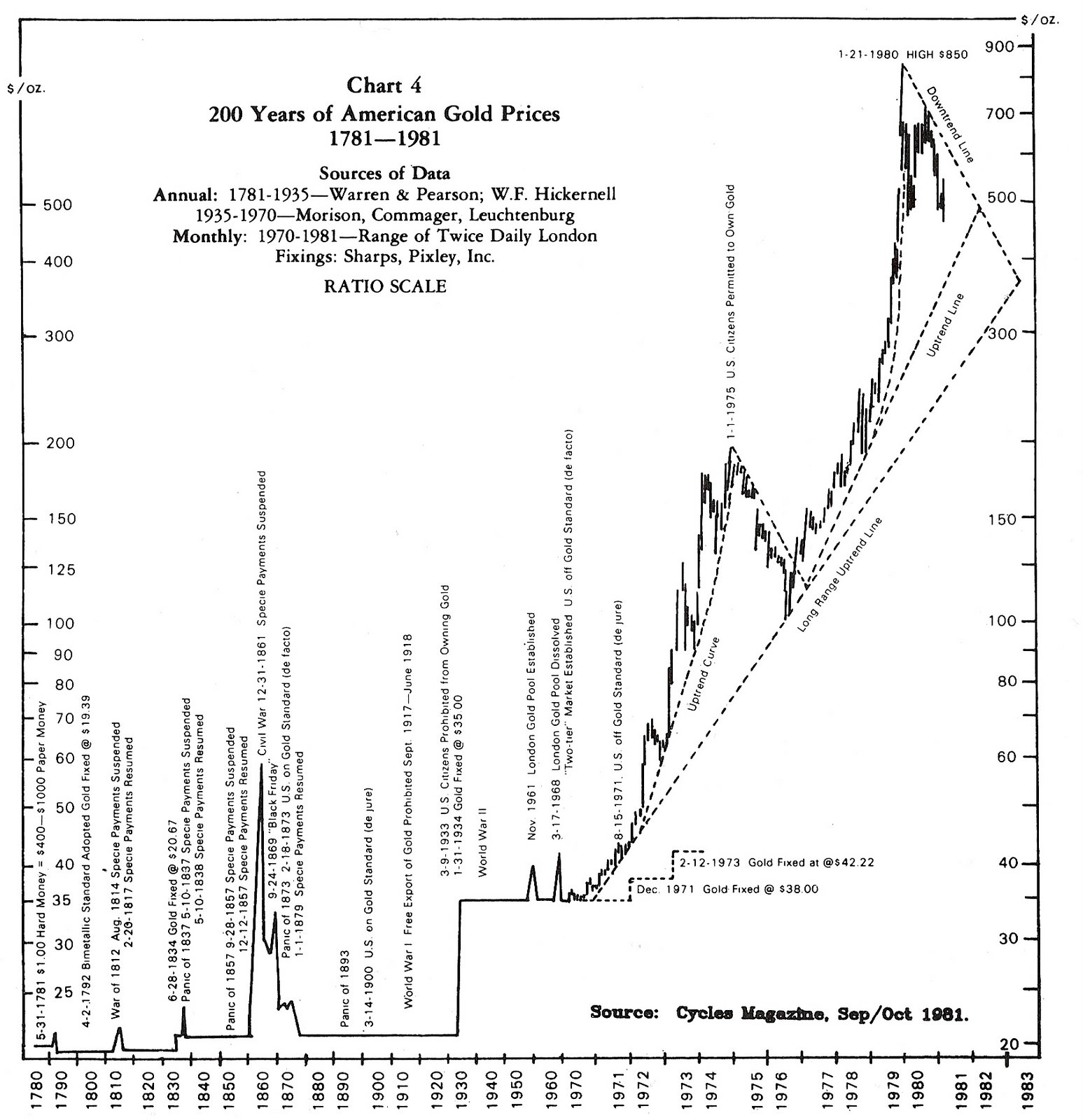

For illustrative purposes, let's start with the bottom of 1932 and compare silver with gold. At the low in 1932, silver was priced as low as $0.24 an ounce. Gold, on the other hand, was fixed at $20.67 per ounce. At the peak of the market in 1980, gold was selling at $800 an ounce while silver was selling at $50 an ounce. During the period from 1932 to 1980, gold went up 3,770% while silver went up 20,730%.

Gold bugs, ever clinging to their religion, would argue that silver was cornered so the $50 figure was a fraud. Gold bugs would also claim that if gold was allowed to freely float during the crisis of 1929-1932 then gold would have been much higher than the price of silver in 1932. These arguments demonstrate a lack of knowledge on how commodity markets work, basic economics and history in one fell swoop.

For the aforementioned reasons, I will calculate the change of silver from $0.24 to $25. Despite halving the figure, silver still achieves an astounding 10,316% increase from the low of 1932. Any way you slice it, the ratios are completely disfigured and in favor of silver. I could have started my pricing point in the 1950's, 1960's or the 1970's and the distortion would be the same but that would be an exercise in futility when talking to a gold bug. Their retort is always the same, "what about this?" or "You're being selective" or "You're biased" or etc. etc. etc. ad infinitum...

Back to me and my silver holdings, when the price of silver has moved in step with the price of gold, on a percentage basis, then I know that silver is underpriced as a precious metal. With this in mind, I converted a majority of my gold holdings into silver. I'm an investor, therefore I don't want to get myself caught up in the religions debates about gold.

So, if (note the size of the if) you're considering taking the dive into gold then move on to the alternative with every bit the attribute. I suggest that you avoid the numismatic varieties of silver. Instead, aim for junk silver of the half dollar denominations. Again, only buy precious metals as part of a balanced diet of physical real estate, stocks, bonds and cash.

In my opinion, gold and silver stocks are perpetual options on the price of gold and silver. Therefore, precious metal stocks are great for speculation but poor investment choices. Be mindful of the coming competitive dividend war between precious metal companies. I remember one, now defunct, gold company that paid out their dividend in actual gold. These are all gimmicks to lure investors in at a time when the rule of the day should be "head to the exits."

If you've read my blog at any length then you already know of the Dividend Achievers that have beat gold and silver stocks without the added risk. However, if you're a hardened equity speculator, you could nab select gold and silver convertible preferreds. Gold and silver equities aren't my first choice but now you know some of the options available to you.

A Note of Caution for All Precious Metal Investors

As the price of the precious metals get higher, the less likely you'll get the widely quoted price when trying to cash in. Precious metal dealers, being business folk, will not be willing or able to take the risk of buying back your gold and silver at the highest quoted price. Therefore, even though gold was at $800 and silver was at $50 back in 1980, investors who tried to cash in at those prices were being turned away by dealers. This will be one of the signs that we're at a top in the market for precious metals.

When you read the following articles on gold and silver, you need to understand that I have a vested interest in the topic. Therefore, I theoretically should say things that only support the investment positions that I retain. Unfortunately, I don't see (revealing my limitations) the value of the philosophy of "whose food I eat, whose song I sing." Additionally, it would be no contradiction that I would explore and write about the breadth of both sides of the topic of precious metals investing. Touc.

related articles:

Please revisit Dividend Inc. for editing and revisions to this post.

{kind=link}