The latest investment observation is on California Water Service Group (CWT). According to Yahoo!Finance, CWT "...engages in the production, purchase, storage, treatment, testing, distribution, and sale of water for domestic, industrial, public, and irrigation uses, as well as for fire protection."

As noted in our Dividend Achiever watch list dated January 1st, CWT is within 10% of the 52-week low. CWT has increased its dividend for 41 years in a row. The 10-year compounded growth rate of the dividend is an anemic level of less than 2%. Keep in mind that with a 41 year history of increased dividends, the odds favor the dividend remaining the same or being cut in the near future. A cut in the dividend would initiate the selling of the stock automatically, regardless of other fundamental attributes.

CWT has had a pattern of trading in a range for approximately 6 years at a time before breaking out to a new and higher trading level. The following are the range in years that CWT traded before obtaining a new high:

-

1976 to 1982

-

1985 to 1993

-

1993 to 1997

-

1997 to 2004

-

2005 to 2011 ???

Because CWT has averaged 6 years before breaking out to a new higher price, we suspect that the current period, after trading in a range for the last 5 years, might provide relatively sizable capital appreciation over the next two and a half years. In addition, because the stock price has been range bound while the dividend has been increased each year, investors can feel comfortable knowing that either of two things are going to happen with the stock 1) the price increases or 2) the dividend yield increases. Either of these scenarios are likely if CWT can retain its overall financial standing.

According to Dow Theory, CWT has the following upside and downside targets.

Upside:

-

$48.29

-

$41.42 (fair value)

Downside:

While we am hopeful of the upside prospects, potential investors need to consider their willingness to hold this stock through the possible downside targets. Personally, we would consider selling the stock if it fell below the $27.40 level. This means that we would be accepting the potential loss of 26% before deciding if we should continue to hold the stock. However, a lot depends on market conditions at the time that CWT falls to the respective downside targets. Our goal is to obtain CWT at a lower price than the current level and sell the stock at or near the $48 level.

To put our investment observation in perspective, IQTrends.com considers CWT undervalued when the stock trades for $16.85. According to Value Line Investment Survey, CWT trades at a mean price of:

- $33.61 based on the 30-year treasury

- $33.98 based on the 20-year treasury

- $40.42 based on the 10-year treasury

Being as conservative as possible, both sources indicate that CWT is overvalued or fairly priced by as much as 54% and as little as 8.71%. In theory, a stock that is "fairly" priced has more of a chance of falling in value rather than increasing in value. Also of concern is the possibility of rising interest rates. It would be challenging to expect that the price of a utility can increase in a potentially rising interest rate environment that we might face in the long term.

As mentioned in our recommendation of AquaAmerica (WTR), although CWT is a water utility and water is critical to life, investors need to understand that companies in this industry aren't a "sure thing." The biggest reason for this is that when, and if, water becomes scarce, government regulators will step in to take over (nationalize) what should otherwise be sold at the most profitable price (thereby curbing wasteful consumption.) There is literally an upside cap on profitability to a company like this due to the critical importance of the resource being sold. Additionally, CWT should be considered a relatively risky stock because of its low daily trading volume. With a 3 month average volume of 100,000 shares, this stock may not be suitable for investors who need ready access to the cash on short notice.

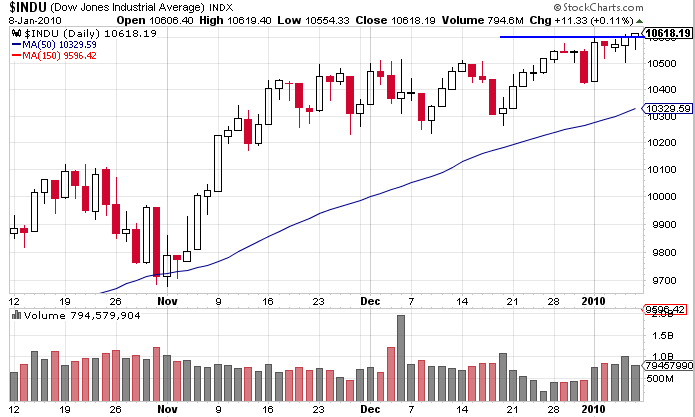

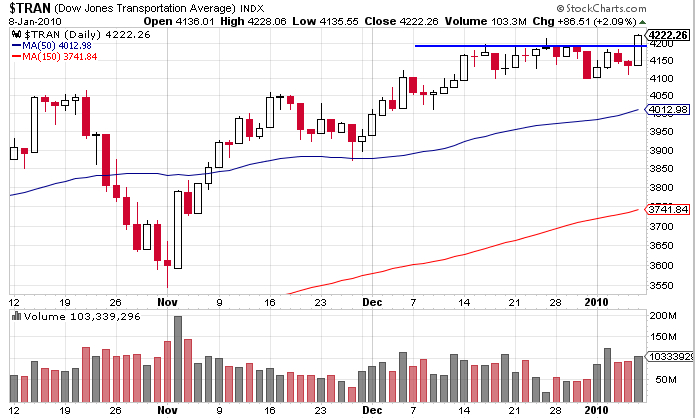

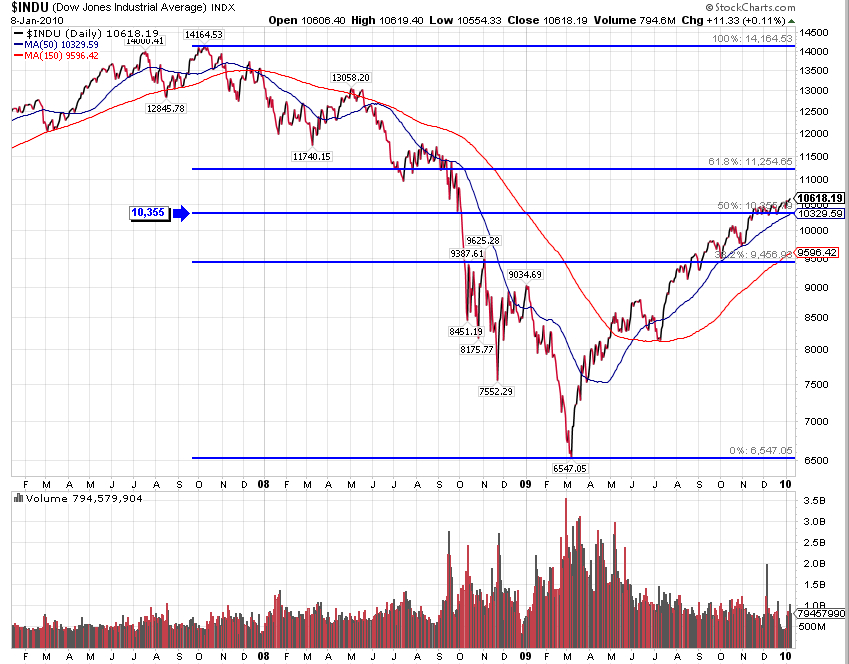

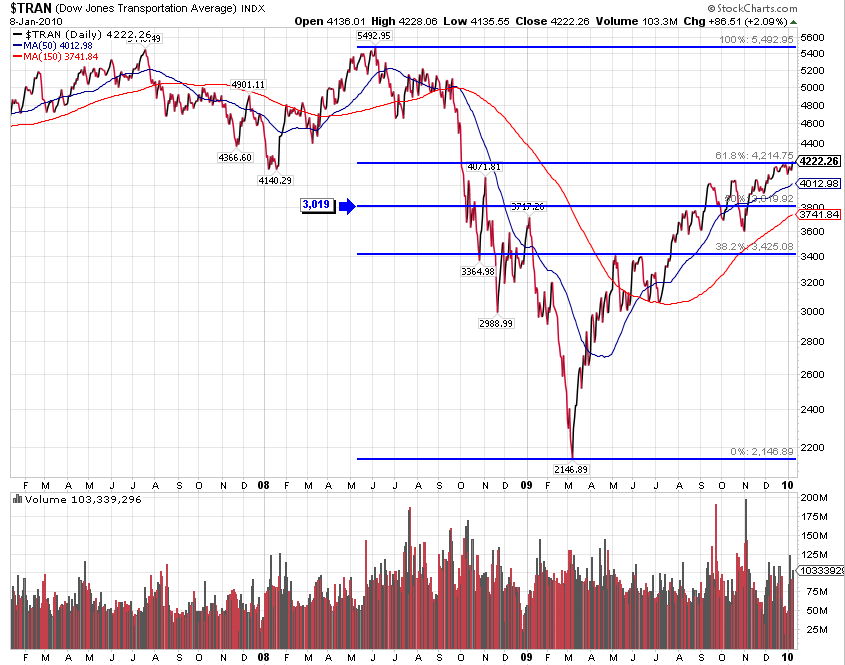

The purpose of our investment observations is to point out quality Dividend Achievers that are near a 52-week low. From this point begins the fundamental research to verify the quality of the stock for both short and long-term investing. These recommendations are within the context of the 3rd year of an 18-year secular bear market. A bear market that we expect could trade in a range between 16,000 and 5,000. The secular bear market will be considered over when the Dow Transports and Dow Industrials exceed their respective peaks on high volume or the dividend yield on the Dow exceeds 6% or higher. -Touc

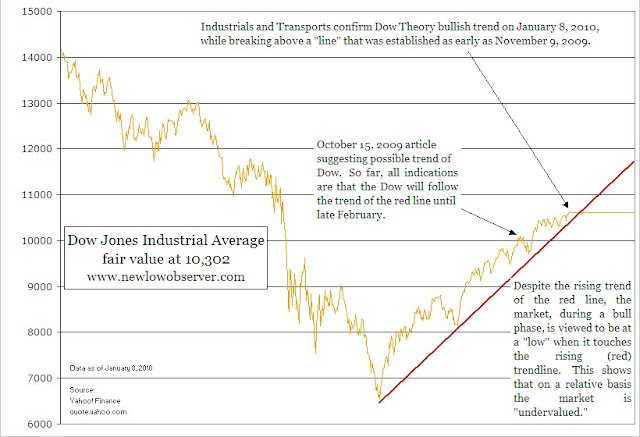

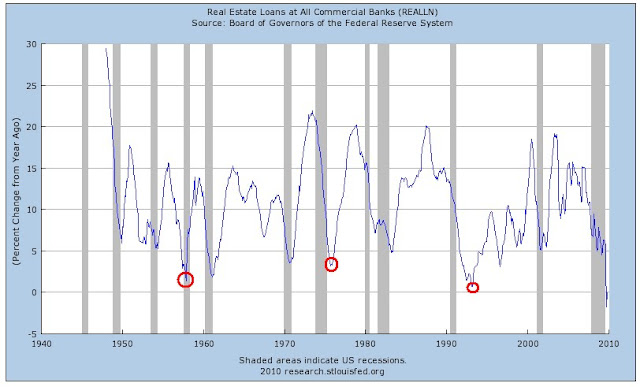

If we haven't hit bottom yet it means that within the year 2010 we will have to go below the previous low prices of 2009. Such an occurrence would be a complete disaster for the financial markets. I am hopeful that the real estate market doesn't further devolve. However, the concern does rest in the back of my mind.

If we haven't hit bottom yet it means that within the year 2010 we will have to go below the previous low prices of 2009. Such an occurrence would be a complete disaster for the financial markets. I am hopeful that the real estate market doesn't further devolve. However, the concern does rest in the back of my mind.

{kind=link}

{kind=link}

{kind=link}

{kind=link}