Edson Gould’s Speed Resistance Lines

On October 25, 2011 (found here), we posted Edson Gould’s speed resistance lines [SRL] for Chipotle Mexican Grill (CMG) and Green Mountain Coffee Roasters (GMCR). So far, the stock price for Chipotle (CMG) has retained considerable strength in the face of extreme market turmoil. However, the situation at Green Mountain Coffee Roasters (GMCR) has completely unraveled.

On November 9, 2011, in after-hours trading, GMCR fell apart by trading as low as $44.02. If we review the [SRL] for GMCR on October 25th (found here), we can see that GMCR was trading around $64 with a conservative downside target of $59.93 and an extreme downside target of $37.21. By falling below the midpoint for the extreme and conservative estimates, we infer that the stock is destined for the $37 level at the minimum. This is the second stock in our survey, after Netflix (NFLX), to adhere to Gould’s speed resistance lines.

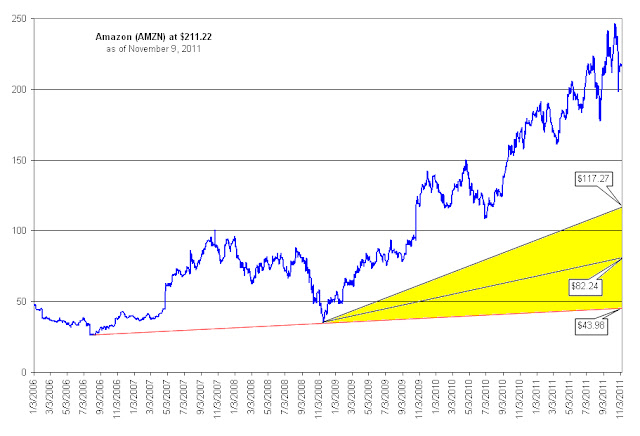

Today we’re adding two new stocks to consider using Gould’s SRL. The first is Amazon.com (AMZN) which currently trades at $211.22. As demonstrated in the chart below, Amazon.com has a conservative downside target of $117.27 with an extreme downside target of $43.98. There is a critical support level of $82.24 that should act as a buffer if AMZN were to actually fall to the $117.27 level.

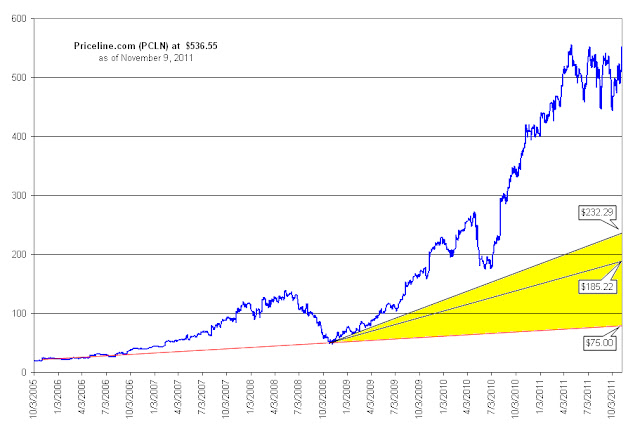

The next stock that we’re watching using Gould’s SRL is Priceline.com (PCLN) which currently trades at $536.55. Priceline.com has been trading in a steady range since the beginning of 2011. However, if that range were broken to the downside, Gould’s SRL suggests that the next downside target for Priceline.com (PCLN) is $232.29 on the conservative side and $75.00 on the extreme side. A substantial support level exists at the 185.22 level which coincides with the low in the stock price in July of 2010.

S.A. Nelson’s View on the “Morality” of Wall Street

The following is an excerpt from the person who coined the term Dow Theory. Considering the rampant distaste for Wall Street, we think it is worth reflecting on Nelson’s words, which, although not popular seem appropriate at this time.

“Perhaps one reason why there is so much disposition to question the morality of Wall Street and contrast it unfavorably with the morality of other business centers is the fact that in Wall Street probably to a greater extent than elsewhere the primal passions and instincts of acquisitiveness and self-preservation wear less disguise than they do in the other channels of industry and money making.“A Stock Exchange anywhere is a theatre in which these primal passions battle as gladiators in the arena without concealment or pretense. Every one who goes down into the arena knows that it is a battle wherein his hand must keep his head, and the penalty of failure will be exacted against him to the utmost. "A la guerre comme a la guerre" (a war as a war) is a proverb that very well describes the conditions under which business is done in Wall Street.“Elsewhere it may appear to be different. The only difference is that in Wall Street there is no pretense, no disguise; the essential struggle is the same everywhere. In Wall Street, there has been and unfortunately still is at times fraud in detail peculiar to Wall Street, but it is not of Wall Street nor inherent in the laws of the game.“It is true that speculation in Wall Street is looked upon as being especially immoral by comparison with speculation elsewhere. It is, however, part of almost every manufacturer's business or of every merchant's business to speculate in raw materials or goods, and nobody thinks of finding fault with either for doing so. In Wall Street speculation stands alone, without any business disguise, for all men to see.”Nelson, Samuel Armstrong. ABC of Stock Speculation. 1902. page 25.

Keep in mind that the preceding thoughts were penned in 1902. Thus adding more evidence to the idea that, “in science knowledge is cumulative, while in finance knowledge is cyclical.” It seems that very little has been learned about the beneficial role that Wall Street has to play in American society.

Greenhill & Co (GHL) Says It Won't Happen

On July 22, 2011 (found here), we made a case for Greenhill & Co. (GHL) to cut their dividend by half. In that missive we said the following:

“Cutting the dividend would put Greenhill & Co. (GHL) in a better financial position to retain the staff necessary to get the mergers and acquisitions done. We recognize that the dividend, with a payout that exceeds current earnings, would further undermine the current stock price and pay less cash to the largest shareholders. However, maintaining such a high dividend leaves less cash available to pass on to their most valuable asset, the employees.”

After falling by 25% since our piece on July 22nd, it seems apparent that action on the dividend is warranted. However, on November 9, 2011 as reported at Bloomberg.com (found here), CEO Scott Bok said:

“‘you’d have to waterboard me’ to persuade [me] to cut the firm’s quarterly dividend.”

Not accounting for Bok’s poor choice of words, we’re disappointed that such a stance only supports the largest shareholders instead of the longer-term interests of the company. It seems that investors in Greenhill & Co. (GHL) have been provided fair warning by the CEO, if you want change it ain’t gonna happen with the dividend.