This website is intended to give new insights on a low risk approach to trading in dividend paying stocks for tax deferred accounts with the ability to buy and sell individual stocks. This website is not intended for regular or non-qualifying accounts however, the strategies and stocks mentioned can be used for non-qualifying accounts with the understanding of the consequences of potential short-term capital gains as well as the need for exceptional documentation for IRS purposes.

The stocks mentioned here are all from past and current Dividend Achievers as published by Mergent's and components of the Nasdaq 100 index. The Dividend Achiever Index of stocks was at one time published by Moody's Investor's Service. Mergent's picked up the Dividend Achievers from Moody's a few years back and has carried on the service of listing companies that have increased their dividend every year for at least 10 consecutive years in a row. The companies mentioned on this website have committed to a policy of rewarding the shareholder with dividend increases without sacrificing the potential for a higher stock price and company growth. It is strongly recommended that readers of this website first find a library that has a copy of Mergent's Dividend Achievers. After reviewing this publication you'll find that you will probably buy this book on an annual basis. Visit Mergent's Dividend Achievers website for additional information about the publication.

Only postings with Investment Observation (IO) before or after the stock name are those that are considered by New Low Observer (NLO) as worthy of being researched and then put on a watchlist and bought at the lowest possible price after the IO. All stocks that are part of NLO's IO will be followed by a sell recommendation. The absence of a sell recommendation means that the stock should be held if it has been purchased. All other stocks that are mentioned are strictly for the purpose of market or stock commentary.

Goal of this Website

When this website makes a IO it will only be in the instance that the observed stock has fallen within 20% of the 52-week (1 year) low. This is intended to bypass the problem faced by momentum investors who buy high and are forced to hold stocks until they "perform" as expected or sell the otherwise unwanted stock at a significant loss. Furthermore, Dividend Achievers allow for traders to substitute an immediate decline with holding the stock while accruing income until the price recovers.

After a stock has fallen within 20% of the 52-week low, NLO will use various means to evaluate a company. Because information about dividend paying stocks is widely available we suggest that you verify if our IO fit your short and long term investment objectives. While NLO is versed in the many ways to evaluate a stock from a fundamental and technical basis, we choose to offer up, from time to time,

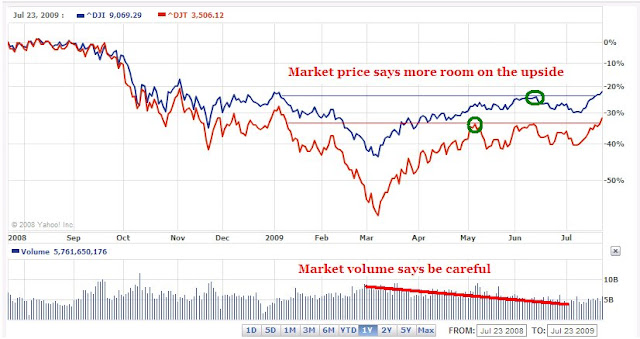

Dow Theory interpretations of what the stock

might do.

The NLO team has no intention of fulfilling the mantra of

diversification. The NLO writers feel that diversification can easily be met by owning a single S&P 500 Exchange Traded Fund (ETF) or Index Fund with low fees. NLO feels that diversification is another word for dilution of gains and reflects an investor's lack of experience and understanding of risk. Ideally, the goal of this website is to have 100% of the investment portfolio broken into fifths, at the most, and invested at all times. However, if the individual stock purchase has achieved the overall goal of exceeding the return on "safe" or "guaranteed" money then a portion or all the funds will be withdrawn from the stock market.

The primary focus of this website is to:

-

maximize the annual return of each trade.

-

reduce time between buying and selling of each stock.

-

exceed the annual yield of government guaranteed alternatives in each trade.

- sell stocks that cut their dividends regardless of gain or loss

NLO does not subscribe to the belief that stocks should be bought and held for the "long term." Ideally, if a return of 17% can be achieved on a third of the portfolio within a six month period of time when U.S. Treasuries are yielding 5% annually then the after-tax gain of 6%-9% is justifiable. The preceding example assumes the money is in a regular or non-tax deferred account. For this reason, stocks that are part of the Investment Observations can be conceivably held as short as a day or as long as 10 years. Suffice to say, we at NLO are comfortable with gains as little as 5% as long as it exceeds the yield on government guaranteed money within a year's time.

Our Investment Strategy

The investment strategy of NLO is quite unorthodox but worth examining.

-

We only hold three stocks at a time. This means that our portfolio is broken into fifths at the most.

-

We try to be fully invested at all times. This presents challenges during bear markets (declines of 30% or more.)

-

We avoid stocks within an industry that has reached a new high.

-

High yield stocks without a dividend history are avoided. High yield often means high risk.

-

A stock is only considered a Investment Observations (IO) when it has fallen within 20% of the 1-year low.

-

Observations are put on a watchlist to be followed until an optimum price has been reached, preferably lower than the IO price.

-

Once a stock is purchased we hold until the gain on the stock doubles that of "guaranteed" money or 10% has been achieved within a 1 year time frame.

-

Stocks that have a gain of 10% or doubled the yield on guaranteed money are considered for a "sell recommendation."

-

As a stock is sold it is suggested that investors revisit the watchlist for the next stock to research.

-

Stocks to consider should be ranked in order of those that have fallen the most since the IO was issued.

-

From this point the stocks that have lost the most are re-evaluated and one is chosen for replacement of the recently sold position.

Ideally, stocks purchased using this method have the benefit of either performing (going up) in a reasonably short period of time or paying the investor for the wait. This method mirrors the "buy for the long term" approach except that it doesn't rely on the hope that the stock price will rise. Buying low(er) ensures that the investor limits the downside risk and maximizes the idea that all "investments" should derive some form of income until the investment is ultimately sold. Conveniently, this investment approach allows an investor to decided when to sell rather than being force to sell due to "buyer's remorse."

Our Team

The current contributors to this website are not registered representatives or a member of any brokers, dealers, market making firm, national or global stock exchanges. Despite our confidence in our recommendations and lacking the credentials necessary to professionally manage money, we must state that this website is for "entertainment purposes" only. We encourage your thoughtful commentary to our site as this is a forum to learn and spread knowledge.

Disclaimer

As a disclaimer, the NLO team is not liable for misunderstandings, misinterpretations, and errors that lead to investment loss. Our research is believed to be from reliable sources that are cited at all times. In the instance that a source is not cited it is done in error. It is best to assume that our team has a conflict of interest due to the fact that we may actually own the stock before the publishing of a IO or we may have sold a stock before a Sell Recommendation. We do not short sell (sell short) or hold put options on any of the Sell Recommendations that are made. Sell Recommendations are not our opinion of the management team of the company in question. Instead, Sell Recommendations are reflections of our opinion that the money invested in a particular stock is better allocated in other stocks.

The companies that are within 10% of the low offer a great opportunity to do research and consider buying.

The companies that are within 10% of the low offer a great opportunity to do research and consider buying.