In attempting to understand Dow Theory it is necessary to follow the best and the brightest on this topic. Over the last 52 years, the brightest person on Dow Theory has been Richard Russell. No single person has been more outspoken on their views on the market using Dow Theory, uninterrupted since 1958, than Richard Russell. So when Richard Russell does an about face on his interpretation of Dow Theory it is worth our time to examine the reasons.

First, it is necessary to provide context around the ideas on Russell’s most recent market call.

- From November 12, 2007 to January 2, 2009, Russell indicated that we were in a bear market. The Dow went from 12,987.55 to 9,034.69, a decline of -30.44%.

- From January 5, 2009 to January 12, 2009, Russell indicated that we were in a bull market. The Dow went from 8,952.89 to 6,926.49, a decline of –22.63%.

- From March 11, 2009 to July 22, 2009, Russell indicated that we were in a bear market. The Dow went from 6,930.40 to 8,881.26, a gain of +28.15%.

- From July 23, 2009 to May 19, 2010, Russell indicated that we were in a bull market. The Dow went from 9,069.29 to 10,444.37, a gain of +15.16%.

- From May 20, 2010 to July 8, 2010, Russell indicated that we were in a bear market. The Dow went from 10,068.01 to 10,138.99, a slight gain was registered for the period (<1%).

On July 9, 2010, Richard Russell said:

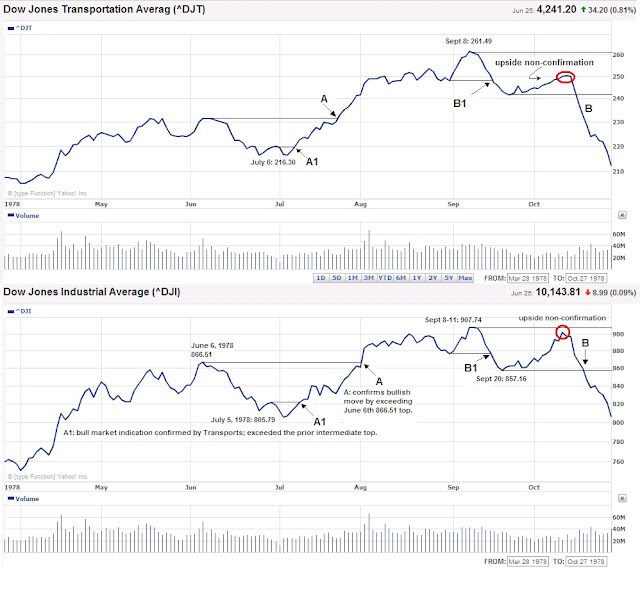

“When the facts change, I change. To do otherwise would be idiotic. Something occurred yesterday that made me sit up and take notice. We had the non-confirmation by the D-J Transportation Average, a situation that I discussed on the July 5 site.”

“Following the Transport non-confirmation, yesterday the market surged higher, Dow up 274 and Transports up 152. But that's not all. What I noticed was that yesterday was a 90% up day [up volume versus down volume] -- the formula for a bottom.”

According to Russell, the Transports non-confirmation along with a 90% up volume/down volume ratio is what led to the conclusion that the market was indicating that a bottom was in. Russell goes on to recommend buying various ETFs with stop losses. Several problems arise when market action is viewed from Russell’s perspective.

First, Russell has ignored the fact that a trend is in place until a counter trend is signaled. So far, we haven’t had a bear market indication since the March 9, 2009 low. If the Transports were to confirm the Industrials by falling below the February 5, 2010 low, then we’d have our first bear market signal.

Second, when thinking in terms of Dow Theory, market participants have three variables to consider the Dow Jones Transportation index, Dow Jones Industrials and NYSE volume. Volume attributes are considered over a period of time. Single day action on volume should not be the determining factor for considering a bull or bear market. If this is the case, then most market signals could be very misleading. In my observations, market volume has increasingly become an addendum to Dow Theory.

Third, Russell has often disregarded the pure Dow Theory indications that have come along the way since the March 2009 low. It seems that Russell’s understanding of macro issues and his personal experience in the markets has led to his decision to err on the side of caution. However, Russell’s cautious streak has usurped the value of Dow Theory to act as a

“…composite index of all the hopes, disappointments, and knowledge of everyone who knows anything of financial matters, and for that reason the effects of coming events (excluding acts of God) are always properly discounted in their movement. The averages quickly appraise such calamities as fires and earthquakes.” (Rhea, Robert,

The Dow Theory, page 19).

Next, Russell has set himself up for the need to change his analysis by not thinking through Dow Theory to its conclusion. By calling a bottom at this juncture, Russell has left out the all-important confirmation that is required by the Industrials and Transports. 10,450.64 and 4,467.25 are the new levels that the Industrials and Transports need to surpass before any buying policy should be considered. In addition, after surpassing the referenced upside confirmation points, the next level of resistance is 8% away for both indexes. This means that we could go to the old high and then quickly reverse to the downside if a bull market confirmation isn’t signaled. However, given the most recent market action, our focus should be on the confirmation of the reversal pattern first, then the possible bull market indication.

Another matter of concern is that Richard Russell makes recommendations that don’t address the issue of investing in values. Values are a core tenet of Dow Theory. In fact, when you read

Dow Theory Unplugged or

Charles H. Dow: Economist, you will find that values, not technicals, are espoused. Russell points his readers to speculative opportunities instead of undervalued stocks which can be held for “the long term” if the bullish assessment happens to be incorrect. Our list of Dividend Achiever stocks at or near a new low addresses the prospect that if we’re wrong there is some recourse. In this case, you get the ability to compound your investment over time with the prospect of capital appreciation.

Finally, our stance on stop loss orders is widely known as indicated in the article “

Automatic Orders Don’t Provide Protection” as well as our disclaimer at the end of each sell recommendation. Russell's recommendation of buying ETFs is reckless at best especially in light of the May 6, 2010 “flash crash.” Adding fuel to the flames is the article titled “

ETF ‘Circuit Breakers’ Needed to Stop Flash Crashes: Pros.” Our stance on ETFs is well founded and preceded any discussion of the true risks associated with them on May 6th (“ETF: Mediocrity With No Pretense of Value” and “ETF: Indiscriminant Risk”).

It is likely that perma-bulls will seize on the Russell commentary of July 9th as the heralding of a new-new era in investing. On the other hand, “contrarian investors” will suggest that when Richard Russell, perma-bear that he is, has entered the bull ring then the bull run is definitely over. It is our contention that while Richard Russell might be right about a reversal pattern being in place he is not using Dow Theory.

Our latest views on Dow Theory can be found at the following link (

NLO on Dow Theory). Keep in mind that all trends are considered to remain in place until otherwise indicated. So far we are still in a cyclical bull market within a secular bear market.