- Japan

- Market Indicator

- Price Momentum Indicators

- Richard Russell

- Silver

- Speed Resistance Lines

- U.S. Dividend Watch List

From what I can tell we need another 3 months of rising numbers along with an increase above -260 for the Coppock Curve to establish a clear signal that a sustainable market reversal is at hand. I know that asking for 3 more months of rising figures seems like a lot. However, I just don't want to get faked out like what occurred in May of 2002. The actual turn in the index took place in March of 2003, almost a full year later. Would I be missing a lot of market "action" by taking this stance? Absolutely. However, the risk to your hard earned principal is what is at stake. It is always best to take the cautious stance on these matters.

Remember, The Coppock Curve is a relative strength index. In almost every instance that this index rises from a negative number to a positive number it has coincided with a relatively risk-free time to invest in stocks. In turn, an improvement in the stock market is a reflection of the better times in the U.S. economy overall. Let us hope that the trend continues. Touc.

Please revisit Dividend Inc. for editing and revisions to this post.

Posted in Coppock Curve, Coppock Index

PBI has many issues that cannot be ignored. The debt situation is not very favorable to the company, especially since PBI provides the financing for their consumers. PBI could have overextended credit on the upswing of the previous cycle and is now getting hit by the double whammy of companies having difficulty paying back their debt as well as a stalled economy that has reduced the demand for their postal equipment. PBI also has a high dividend payout ratio of 73% based on trailing twelve months earnings.

My expectation is that PBI will fall further when the market opens. As long as the Dow Theory bull market indication isn't reversed and depending on the extent of the decline, I would consider buying PBI. Of course, I'm hoping for a situation where the price goes all the way down to the $14 or $15 level established in 1992. I strongly recommend that you watch this stock and do your research. Touc.

Please revisit Dividend Inc. for editing and revisions to this post.

Posted in Achiever Alert, Fibonacci, PBI

Please revisit Dividend Inc. for editing and revisions to this post.

Comments Off on Congrats to Terry

Posted in Uncategorized

"U.S. equity exchanges have catered to such clients since at least 1997, when the NYSE ended its century-old practice of quoting stocks in eighths of a dollar. It shifted to penny increments in 2000. That eroded earnings for NYSE and Nasdaq market makers, who profit from the difference between bids and offers. For investors, it helped reduce trading costs.

The exchanges sought to compensate for the lost business by paying rebates to high-frequency brokerages that buy shares at the best public prices. Exchanges have also overhauled their trading systems to cut transactions times and rent space in data centers so it takes less time to transmit information to buyers and sellers. Bats Global Markets processes orders in less than 400 microseconds, or 0.0004 second, which is about 1,000 times faster than humans blink their eyes."

Edgar Ortega, Jeff Kearns and Eric Martin. "High-Frequency Traders Say Speed Works for Everyone." Bloomberg.com. July 28, 2009. accessed July 29, 2009.

This issue of stocks trading in pennies instead of eighths is critical to the increased manipulation of the stock market. This was a specific matter that I raised in my March 16th posting.

Also, in the comment section of the same March 16th posting, I got a great question about the effectiveness of limit orders and stop loss orders. As I said at the time, your only tool for avoiding the maximum amount of market manipulation is to place market orders. As early as August 12, 2008 in my sell recommendation of Helmerich and Payne, I stated that only market orders should be used to avoid manipulation. Any individual investor who uses automatic orders as a form of "protection" is really subjecting themselves to greater losses and diminished gains. You heard it here first. Touc.

Please revisit Dividend Inc. for editing and revisions to this post.

Comments Off on Concerned About Market Manipulation?

Posted in Automatic Orders, Goldman Sachs, manipulation, pennies, short selling, uptick rule

It is always recommended that when selling a stock, one should not place an order after hours or when the market is closed. This leaves the seller in the position of being vulnerable to the whims of the market makers. Instead, place your sell orders only as a market order during market hours. Some would complain that a market order during market hours might leave some profits on the table. However, I would rather leave some money on the table rather than have it taken away from me by the trades that are placed by institutions and market makers. Touc.

Please revisit Dividend Inc. for editing and revisions to this post.

This blog is being featured on www.condron.us, I hope you find this useful.

Comments Off on Sell Cardinal Health (CAH) at the Market

Posted in CAH, Cardinal Health, Sell Recommendations

When William Peter Hamilton 17 years ago, wrote the first book on the Dow theory he called The Stock Market Barometer, not because of the theory's value in forecasting the course of stock prices, but because of its value as a barometer of business. Most of the literature on the theory written since then has concentrated on technical studies of its method of identifying stock market trends, both bull and bear, shortly after their beginning.In this book Rhea returns to Hamilton's original thesis, at which he pounded away steadily in his editorials in The Wall Street Journal and in comments in Barron's up to the time of his death in 1929. But whereas Hamilton had to depend on observation, Rhea has contributed to this subject the first detailed comparison of all the Dow theory bull and bear market signals back to 1897 with the movements of Barron's business index over the same period.

Rhea is well known as author of Dow Theory Comment, comprising air mail letters attempting to forecast stock and business trends; The Dow Theory, an introduction to the theory together with a complete collection of all of Hamilton's discussions of the price movement; and The Story of the Averages, a play-by-play history of every bull and bear market signal the averages have given since their inception and of the course of the market over the whole period. It is from this work that the Dow theory signals used in the new book are taken.

Business Book of the Week. Barron's. October 31, 1938. page 9

Comments Off on Reader Appreciation Day

Posted in Reader Appreciation Day

As you read through the book you'll find that the head of Lehman, Richard Fuld, resisted all efforts to keep the company afloat. The mistaken belief by Fuld that he could easily avoid failure because of the prior bailout of Bear Stearns (otherwise known as moral hazard) is what led to the ultimate fall of Lehman. Additionally, it didn't help that while Paulson and Bernanke were trying to create sweetheart exit strategies for Lehman, Fuld maintained an "in-your-face" my way or the highway attitude.

As a sidebar, my comment that Bank of America "must really be in trouble" was precient considering that on September 15, 2008 the stock closed at $25.86. Even after rising 295% from the March 6, 2009 low, Bank of America is still trading 51.62% below the September 15th price. My September 14th thoughts on Bank of America got me to wondering where the company was headed so I did a Dow Theory analysis of BAC the very next day. I highly recommend that you re-read my analysis of BAC, it is well worth your time. Touc.

Comments Off on

Posted in Bank of America, Lehman, Richard Fuld

Comments Off on Investment Observations

Posted in Uncategorized

Comments Off on Speculation Observations

Posted in Uncategorized

The companies that are within 10% of the low offer a great opportunity to do research and consider buying.

The companies that are within 10% of the low offer a great opportunity to do research and consider buying.

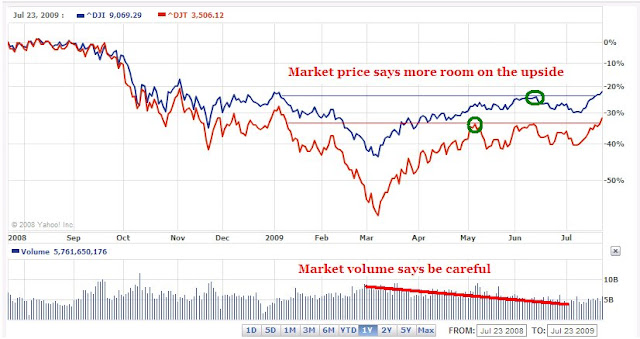

Based on the fact that both indexes went to new highs on the same day would normally mean that we are in a new bull market. However, because Dow Theory considers trading volume as well as price, the fact that trading volume has been declining throughout the most recent price rise means that there isn't broad participation by either institutional or retail investors. Therefore, I would label this a cyclical bull market which can change direction to the downside without warning.

Based on the fact that both indexes went to new highs on the same day would normally mean that we are in a new bull market. However, because Dow Theory considers trading volume as well as price, the fact that trading volume has been declining throughout the most recent price rise means that there isn't broad participation by either institutional or retail investors. Therefore, I would label this a cyclical bull market which can change direction to the downside without warning.Comments Off on Dow Theory

Posted in Dow Theory, Dow Theory Bull Market indication

NLO does not subscribe to the belief that stocks should be bought and held for the "long term." Ideally, if a return of 17% can be achieved on a third of the portfolio within a six month period of time when U.S. Treasuries are yielding 5% annually then the after-tax gain of 6%-9% is justifiable. The preceding example assumes the money is in a regular or non-tax deferred account. For this reason, stocks that are part of the Investment Observations can be conceivably held as short as a day or as long as 10 years. Suffice to say, we at NLO are comfortable with gains as little as 5% as long as it exceeds the yield on government guaranteed money within a year's time.

Our Investment Strategy

The investment strategy of NLO is quite unorthodox but worth examining.

Ideally, stocks purchased using this method have the benefit of either performing (going up) in a reasonably short period of time or paying the investor for the wait. This method mirrors the "buy for the long term" approach except that it doesn't rely on the hope that the stock price will rise. Buying low(er) ensures that the investor limits the downside risk and maximizes the idea that all "investments" should derive some form of income until the investment is ultimately sold. Conveniently, this investment approach allows an investor to decided when to sell rather than being force to sell due to "buyer's remorse."

Our Team

The current contributors to this website are not registered representatives or a member of any brokers, dealers, market making firm, national or global stock exchanges. Despite our confidence in our recommendations and lacking the credentials necessary to professionally manage money, we must state that this website is for "entertainment purposes" only. We encourage your thoughtful commentary to our site as this is a forum to learn and spread knowledge.

Disclaimer

As a disclaimer, the NLO team is not liable for misunderstandings, misinterpretations, and errors that lead to investment loss. Our research is believed to be from reliable sources that are cited at all times. In the instance that a source is not cited it is done in error. It is best to assume that our team has a conflict of interest due to the fact that we may actually own the stock before the publishing of a IO or we may have sold a stock before a Sell Recommendation. We do not short sell (sell short) or hold put options on any of the Sell Recommendations that are made. Sell Recommendations are not our opinion of the management team of the company in question. Instead, Sell Recommendations are reflections of our opinion that the money invested in a particular stock is better allocated in other stocks.

Comments Off on About This Site

Posted in Uncategorized

I have followed Apple for many years and I can't seem to understand why investors continue to allow themselves to be taken again and again without pause. Apple is replete with examples of how the company has managed to game the system. I will point out the glaring examples that can be proven and hope that others will allow for the facts to stand juxtapose to the exciting stories that have been created to fan the destructive flame of an adoring public. Below are my top five reasons why I can't trust the way Apple operates as a company.

Problem 1: Option Repricing

Since its IPO, Apple Computer had been the innovator of “serial option repricing.” This method allowed Apple to continually reprice the stock options as the shares of Apple stock fell. This is unique since most companies would reprice their options only one time after the price fell below the exercise price. In the case of Apple, the options would be continually repriced as the stock went on a downward decline. This is critical since Apple has used options as the primary means of compensation in the executive suite as well as for frontline employees.

It is worth noting that Steve Jobs garners an annual salary of $1. It’s not because Steve Jobs is Mr. Benevolent , instead he is compensated through the value of the options that are issued to him. If the stock price starts to decline then Jobs would be out the value he could have received if he exercised the options at a higher price. This creates the perverse incentive to adjust the strike price of the options lower if the stock goes down.

While the debate of the use of stock options as a form of compensation has died down it should be noted that as early as 1998 the critics of such instruments were vociferous about the risks associated with them. Warren Buffett’s business partner Charlie Munger said that, “stock options resemble ‘a chain letter.’” According to Dennis Beresford, former chairman of the Financial Accounting Standards Board (FASB), options are similar to a “Ponzi scheme.” And like Bernard Madoff’s scheme, the game really starts to fall apart when a sustained decline ensures.

Source: Welles, Edward O. "Motherhood, apple pie & stock options. " Inc. Magazine. Feb 1998.

Problem 2: Management Compensation

During the days of when Gil Amelio was CEO, the board at Apple granted tremendous leeway in how it chose to compensate the CEO. At the time, Apple was expected to lose money for many quarters. How did the board at Apple circumvent this problem to give Amelio the most compensation? The board allowed the company to pursue a strategy of projecting larger losses in the future than was realist and then beating the lose projections. From this standpoint, the board would reset the compensation markers for when the CEO would be able to receive their bonus based on quarterly performance on top of their ordinary pay. This meant that regardless of the number of quarters that had passed without profitability, the CEO was going to receive a bonus no matter what happened. This strategy is similar to what happened to Fannie Mae when the company was forced to restate their earnings and fire CEO Franklin Raines.

Source: Crystal, Graef. "One bad Apple doesn't spoil a whole bunch of stock options. " San Francisco Business Times. Jan 31, 1997.

Problem 3: CEO Bailing

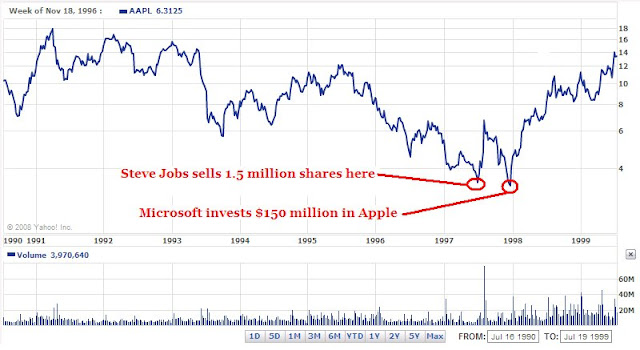

In the chart below you'll see that on June 26, 1997, when Apple was in the throes of a death spiral in the stock price, Steve Jobs decided to sell 1.5 million shares of Apple stock.  This would seem to be the time when the CEO should be trying to “inspire” confidence in the company stock. Instead, Jobs chose to sell his shares just after selling his NeXT Software to Apple for $6.50 a share earlier in the same year. Not long afterwards Microsoft (MSFT) inject a large amount of money into Apple. At that point, Apple shares started to rise tremendously.

This would seem to be the time when the CEO should be trying to “inspire” confidence in the company stock. Instead, Jobs chose to sell his shares just after selling his NeXT Software to Apple for $6.50 a share earlier in the same year. Not long afterwards Microsoft (MSFT) inject a large amount of money into Apple. At that point, Apple shares started to rise tremendously.

Source: Mardesich, Jodi, and Chris Schmitt. "Jobs admits selling shares. " San Jose Mercury News. August 12, 1997.

Problem 4: Slight of Hand

Another problem is that Apple always gives conservative guidance on their projections and always seems to beat expectations by a wider than expected margin. This was a strategy that was employed by General Electric (GE) until it could not sustain the lie of earnings management due to the collapse of GE Capital. GE was able to convince the public that all was well with the way they operates. Even convincing management junkies that Jack Welch’s Six Sigma was the reason for the company’s success. Instead, it was the practice of managing expectations and a little accounting mumbo-jumbo that kept things moving.

Did you notice that the analysts who cover Apple stock continually get the numbers wrong. When I compared the analysts estimates tracking Ebay, Cisco, Google, Adobe and Apple I found that Apple was always off target by a wide margin. In the data below, the last five years analysts estimating the annual earnings were below the target numbers as follows:

In the last five quarters, analysts were off of the target numbers as follows:

The relatively huge disparity between analyst estimates for Apple and other “high flyer” tech companies is cause for alarm. How is that Apple projections are off by nearly 100% as compared to other tech companies that are subjected to the same economic downturn in the economy? Either the analysts aren't getting it right or Apple is managing the situation. From the prior track record of Apple, I suspect that the earnings are being managed to the Nth degree.

Note: The preceding annual and quarterly numbers are derived from ThompsonReuters as of July 15, 2009.

Problem 5: Backdating Options

In 2001, Apple was called to task for the issuance of, among other things, a 7.5 million options grant to Steve Jobs. The problem with this is that the issuance, made by Chief Counsel Nancy Heinen, was dated two months prior to the date actually created. Heinen was later fired from Apple and fined for her role in the illegal activity but it didn't seem that Steve Jobs had any problem with the action until the SEC started doing an inquiry into the unusual backdating of the options. Strangely, the Apple board, "exonerated Jobs---in part because Jobs 'did not appreciate the accounting implication' of backdating."

It seems strange that Heinen would benefit Mr. Jobs and later get thrown under the bus. It is interesting to note that the Apple board said that Steve Jobs didn't know the implications of such actions even though the board "admitted to frequent backdating." If Apple had as a practice the backdating and repricing of options since its IPO, then Steve Jobs should have known as the CEO, the implications, from an accounting and legal basis, the actions being taken.

Again, like every good scheme, the act of backdating options didn't come up as an issue until the blowup of the tech sector. Had the Nasdaq stocks continued to move higher I don't think any of the SEC actions would have been taken on the matter of backdating or repricing of options.

Source: Burrows, Peter. Parting Shots at Apple's Jobs; Former CFO Fred Anderson reached a settlement with the SEC over options backdating--but says the CEO deserves part of the blame. Business Week Online. April 26, 2007.

While the products that Apple create are great for the gee-whiz hipster crowd of the new millennium the actions of the board of directors and executive suite has been questionable at best. As far as I can tell, Apple hasn't cleared the air about the way they have managed the company in the past to justify buying or holding the stock right now. Touc.

Comments Off on Apple Computer: Can’t Trust It

Posted in AAPL, Apple Computer, backdating, Bernard Madoff, repricing, SEC