Our watch list this week contains 22 companies that are within 10% of their 52-week low.

February 25, 2011 Watch List

| Symbol | Name | Price | % Yr Low | P/E | EPS (ttm) | Dividend | Yield | Payout Ratio |

| RBCAA | Republic BanCorp., Inc. | 17.21 | 2.44% | 5.57 | 3.09 | 0.57 | 3.31% | 18% |

| SYY | Sysco Corp. | 27.91 | 2.88% | 14.39 | 1.94 | 1.04 | 3.73% | 54% |

| CWT | California Water Service | 35.13 | 3.90% | 18.59 | 1.89 | 1.23 | 3.50% | 65% |

| PPL | PP&L Corporation | 24.81 | 4.46% | 11.43 | 2.17 | 1.40 | 5.64% | 65% |

| MRK | Merck & Co., Inc | 32.19 | 4.85% | 9.41 | 3.42 | 1.52 | 4.72% | 44% |

| JNJ | Johnson & Johnson | 59.64 | 4.89% | 12.48 | 4.78 | 2.16 | 3.62% | 45% |

| HCBK | Hudson City Bancorp, Inc. | 11.38 | 5.37% | 10.44 | 1.09 | 0.60 | 5.27% | 55% |

| PEP | PepsiCo Inc. | 63.6 | 5.44% | 16.22 | 3.92 | 1.92 | 3.02% | 49% |

| WABC | Westamerica BanCorp. | 51.8 | 6.37% | 16.14 | 3.21 | 1.44 | 2.78% | 45% |

| LLY | Eli Lilly & Co. | 34.09 | 6.46% | 7.44 | 4.58 | 1.96 | 5.75% | 43% |

| CL | Colgate-Palmolive Co. | 78.12 | 6.84% | 18.13 | 4.31 | 2.12 | 2.71% | 49% |

| ABT | Abbott Laboratories | 47.64 | 6.84% | 16.09 | 2.96 | 1.92 | 4.03% | 65% |

| MCY | Mercury General Corp. | 40.62 | 7.18% | 14.61 | 2.78 | 2.40 | 5.91% | 86% |

| AWR | American States Water Co. | 33.68 | 7.81% | 22.91 | 1.47 | 1.04 | 3.09% | 71% |

| WMT | Wal-Mart Stores, Inc. | 51.75 | 8.33% | 11.60 | 4.46 | 1.21 | 2.34% | 27% |

| TGT | Target Corp. | 52.36 | 8.56% | 13.71 | 3.82 | 1.00 | 1.91% | 26% |

| FCBC | First Community Bancshares | 12.52 | 8.87% | 10.18 | 1.23 | 0.40 | 3.19% | 33% |

| CAG | ConAgra Foods, Inc. | 23.00 | 9.42% | 15.44 | 1.49 | 0.92 | 4.00% | 62% |

| NWN | Northwest Natural Gas Co. | 46.05 | 9.90% | 16.39 | 2.81 | 1.74 | 3.78% | 62% |

| KMB | Kimberly-Clark Corp. | 65.08 | 9.97% | 14.62 | 4.45 | 2.80 | 4.30% | 63% |

| WEYS | Weyco Group, Inc. | 24.58 | 10.27% | 21.37 | 1.15 | 0.64 | 2.60% | 56% |

| VLY | Valley National BanCorp. | 13.67 | 10.87% | 16.88 | 0.81 | 0.72 | 5.27% | 89% |

| 22 Companies | ||||||||

Watch List Summary

On the top of our list this week is Republic Bancorp (RBCAA). It is a small regional bank with market cap of just $360 million. The company has an impressing record of dividend payments even through the financial crisis (see chart). Despite the turmoil in the market, it managed to keep the payout ratio below 40%. The highest that figure came was in 2007 at 37%. Republic Bancorp may worth looking into.

Next on our list is Sysco (SYY), a distributor to the food service industry. Our guess is that the stock has been hit by the high food costs and the inability to pass such costs on to customers. What the market may be overlooking is the short-term fundamentals versus the longer-term viability. As recent as last month Sysco raised their dividend payout by 4%. This is an indication that company management believes that, despite the high food prices, prospects for Sysco aren't as dire as people may believe.

After topping our list two weeks ago, Abbott (ABT) rose 4.5%.

Top Five Performance Review

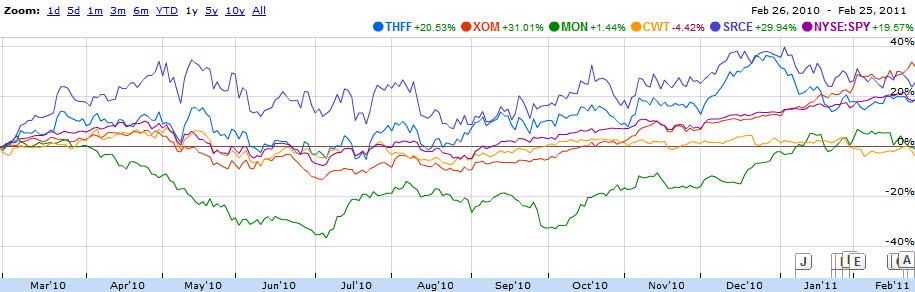

In our ongoing review of the NLO Dividend Watch List, we have taken the top five stocks on our list from February 26, 2010 and have check their performance one year later. The top five companies on that list can be seen in the table below.

| Symbol | Name | 2010 Price | 2011 Price | % change |

| THFF | First Financial Corp. | 26.28 | 32.22 | 22.60% |

| XOM | Exxon Mobil Corp. | 65.00 | 85.34 | 31.29% |

| MON | Monsanto Co. | 70.65 | 72.21 | 2.21% |

| CWT | California Water Service | 35.88 | 35.13 | -2.09% |

| SRCE | 1st Source Corp. | 14.93 | 19.4 | 29.94% |

| Average | 16.79% | |||

| DJI | Dow Jones Industrial | 10,325.26 | 12,130.45 | 17.48% |

| SPX | S&P 500 | 1,104.49 | 1,319.88 | 19.50% |

The performance of our top five stocks were not as impressive as the overall market. California Water (CWT) and Monsanto (MON) held our list to a 16% average gain. Monsanto took a big hit mid-year when the company reduced earning guidance mid year. The shares tumbled and nearly marked the -40% zone as seen in the chart. Investors who went against the tide and bought Monsanto in June/July were handsomely rewarded.

Disclaimer

On our current list, we excluded companies that have no earnings. Stocks that appear on our watch lists are not recommendations to buy. Instead, they are the starting point for doing your research and determining the best company to buy. Ideally, a stock that is purchased from this list is done after a considerable decline in the price and extensive due diligence. We suggest that readers use the March 2009 low (or the companies' most distressed level in the last 2 years) as the downside projection for investing. Our view is to embrace the worse case scenario prior to investing. A minimum of 50% decline or the November 2008 to March 2009 low, whichever is lower, would fit that description. It is important to place these companies on your own watch list so that when the opportunity arises, you can purchase them with a greater margin of safety. It is our expectation that, at the most, only 1/3 of the companies that are part of our list will outperform the market over a one-year period.

{kind=link}